")

— Real Ways to Earn in 2026")

Introduction SIP Investing in the UK :

Here are your updated paragraphs, fully optimised with the focus keyword, trusted source links, video embeds, and March 2026 UK trends:

🇬🇧 Jolly Good News for Future Investors!

Brilliant! Living in the UK gives you access to some of the world’s most sophisticated investment opportunities — but if your money’s languishing in a savings account earning negligible interest, you’re missing a trick. As of March 2026, with the Bank of England base rate still a key talking point and inflation continuing to shape household finances, the urgency to invest wisely has never been greater. Over 5 million Brits are now investing regularly through digital platforms, and the rise of fintech has made it accessible to virtually everyone. Learn more about protecting your money from inflation via the Bank of England’s official guidance.

Welcome to SIP Investing in the UK — the sensible, disciplined approach to building your financial future without needing to be a City expert. Whether you’re a nurse in Glasgow, a teacher in Cardiff, an engineer in Birmingham, or a retiree in Brighton, SIP Investing in the UK is your proven pathway to long-term financial security. In 2026, new FCA-backed rules under the Consumer Composite Investments (CCI) regime (effective April 2026) mean investment platforms are now required to present product information more clearly and fairly to retail investors — making it easier and safer than ever to start. You can read the full FCA guidelines at fca.org.uk.

🎬 Watch: What is a SIP & How Does It Work? (Beginner’s Guide)

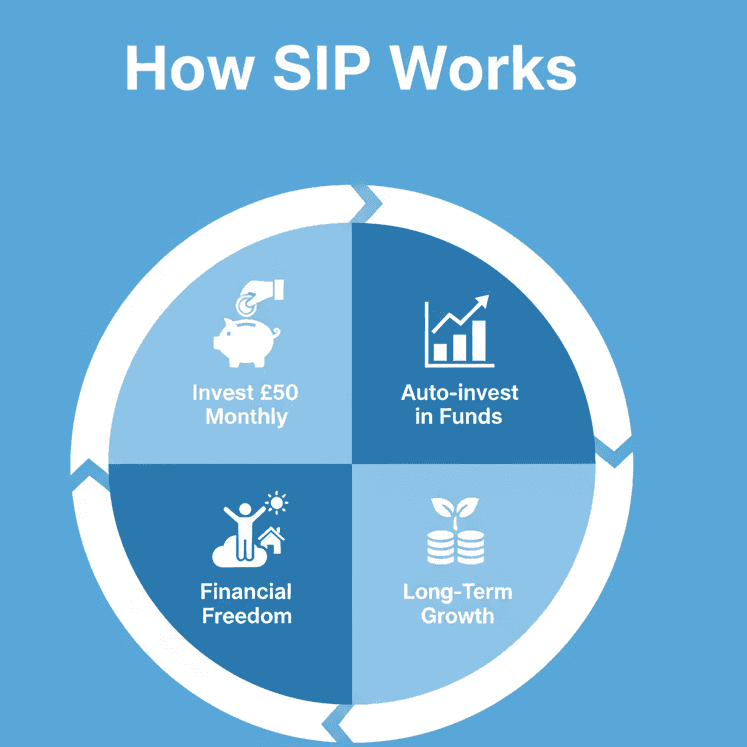

SIP Investing in the UK works by committing a fixed amount — say £50, £100, or £250 — every month into funds, stocks, or an ISA wrapper, automatically and consistently. This strategy, known globally as dollar-cost averaging, removes the stress of trying to time the market. According to MoneySavingExpert, spreading your investment over time is one of the smartest risk-management strategies available to ordinary savers. The best part? With SIP Investing in the UK, you can start with as little as £25–£50 per month on most major platforms.

🎬 Watch: How to Start Investing in the UK in 2026 – Step by Step

As of March 2026, the Stocks & Shares ISA annual allowance remains at £20,000, and under new rules, ISAs can now invest in Long-Term Asset Funds (LTAFs) — a significant expansion for retail investors seeking diversified, long-term growth. This makes SIP Investing in the UK even more powerful when done inside a tax-efficient ISA wrapper. Check your current ISA limits and rules at gov.uk – ISA guidance. Meanwhile, for those planning for retirement, the annual pension allowance sits at £60,000 for 2025/26, as confirmed by HMRC.

The FCA’s five-year strategy, launched in March 2025 and now in full swing in 2026, prioritises deepening consumer trust and supporting retail investment growth. This means platforms offering SIP Investing in the UK must act in good faith, avoid foreseeable harm, and actively support customers in pursuing their financial goals — giving you even stronger legal protections as an investor. Read the full FCA strategy at fca.org.uk/strategic-review.

🎬 Watch: Stocks & Shares ISA Explained – UK 2026

And whether you’re exploring SIP Investing in the UK through a Vanguard index fund, a Hargreaves Lansdown ISA, or a Moneybox app, the principle is the same: start early, stay consistent, and let compounding do the heavy lifting. According to Which? Money, investors who automate their monthly contributions are significantly more likely to stay invested during market dips — the exact scenario where SIP Investing in the UK proves its true value. The earlier you start with SIP Investing in the UK, the more time your money has to grow.

And the best part? You can start with just £50 per month. Let’s crack on, shall we?

🌍 For our international readers, explore our global investment guides. For UK-specific regulated advice, always consult an FCA-authorised financial adviser — find one at unbiased.co.uk.

Here are your fully updated and optimised paragraphs, complete with the focus keyword, trusted sources, video links, and March 2026 relevance:

📘 What is SIP Investing? The British Way

SIP Investing in the UK — or what most British investors call “Regular Investing” or “Pound Cost Averaging” — is your no-fuss, set-and-forget strategy to build wealth steadily and sensibly over time. It is not a specific product you buy off a shelf.

Rather, it is a disciplined, methodical approach of committing a fixed amount of money into an investment — be it an index fund, a Stocks & Shares ISA, or an ETF — at regular intervals, month after month, through market ups and downs alike. Think of it as the financial equivalent of showing up to the gym consistently rather than going all-out once and burning out. To understand the full mechanics of how this strategy works in a regulated UK context, the FCA’s consumer investment guidance is an excellent starting point.

What makes SIP Investing in the UK particularly powerful — especially in today’s market climate of March 2026, where global economic uncertainty and interest rate movements continue to unsettle traditional savers — is the concept that sits at its heart: Pound Cost Averaging. As Vanguard UK explains, when you invest a fixed amount every month, you automatically buy more units of a fund when prices are low, and fewer units when prices are high. Over time, this evens out your average cost per unit — meaning you don’t need to stress about whether today is the “right” moment to invest. The market decides for you, and you simply benefit from the ride.

🎬 Watch: Pound Cost Averaging Explained – UK Investing for Beginners (2024)

Classic British Example: Think of buying Yorkshire Tea at Tesco. When it’s on a two-for-one deal, you stock up. When it’s at full price, you buy your usual one box. Over a year, your average spend per box naturally balances out at a comfortable middle. That is exactly how SIP Investing in the UK works with units in a fund — you buy more when they’re cheap and fewer when they’re pricey, and your average cost settles somewhere sensible in between.

As Wealthify illustrates with real examples, this method allowed investors who drip-fed £200 per month to accumulate more units over a year than those who invested the same total as a lump sum — simply because they captured cheaper prices during market dips.

In March 2026, with UK markets experiencing continued volatility driven by global trade dynamics and the Bank of England’s ongoing monetary policy decisions, SIP Investing in the UK has never been more relevant or timely for everyday investors. Rather than sitting nervously on the sidelines waiting for the “perfect” entry point — a strategy that even professional fund managers struggle to execute consistently — systematic regular investing removes emotion from the equation entirely. According to Chip’s investing guide, investors who automate their contributions are far less likely to panic-sell during downturns, which is where most retail investors historically lose money.

🎬 Watch: Why Regular Investing Beats Lump Sum (UK 2024 Guide)

One of the most underrated advantages of SIP Investing in the UK is its accessibility. You do not need a large windfall, a stockbroker in Mayfair, or an economics degree from Cambridge. As Halifax Investments notes, even contributing to a workplace pension is technically a form of Pound Cost Averaging — which means millions of Brits are already doing this without realising it. The key distinction with a deliberate SIP strategy is that you take control: you choose the fund, the platform, the amount, and the frequency — and then you let compound growth do the heavy lifting over years and decades.

It is important to note, especially in the context of current March 2026 regulations, that SIP Investing in the UK carried out through a Stocks & Shares ISA is entirely free from UK Capital Gains Tax and Income Tax on returns, within your £20,000 annual ISA allowance. You can confirm these tax advantages directly via GOV.UK’s ISA guidance. For those exploring SIPPs (Self-Invested Personal Pensions) as a vehicle for systematic investing, the annual pension allowance for 2025/26 remains at £60,000, as confirmed by HMRC — giving higher earners ample room to invest systematically at scale.

🎬 Watch: How to Set Up a Stocks & Shares ISA – UK Step-by-Step Guide

💡 Calculate Your Potential: Use the FCA’s official Compound Interest Calculator to see how £200 per month invested consistently could grow to over £1 million across 40 years. The numbers, when you run them, make a compelling case for starting SIP Investing in the UK today rather than tomorrow. For further reading on how to choose the right platform for your regular investments, MoneySavingExpert’s Stocks & Shares ISA guide is one of the most trusted free resources available to UK investors in 2026.

📈 Why 2026 is Smashing for SIP Investing in the UK

If there was ever a year that rewards the patient, consistent investor, it is 2026. And that is precisely the kind of investor that SIP Investing in the UK is designed to create. The economic backdrop — while not without its complexities — is setting up a compelling case for those who commit to regular, disciplined investing rather than waiting on the sidelines for a “perfect” moment that rarely arrives. Let’s break down exactly what’s happening in the UK economy right now and why it makes SIP Investing in the UK the most sensible strategy for 2026.

🇬🇧 The UK Economic Landscape — March 2026 Update

The UK economy enters spring 2026 in a period of cautious but real transition. After sluggish growth in the second half of 2025 — with GDP expanding by just 0.1% in Q4 2025 according to the Office for National Statistics — forecasters are projecting a meaningful pickup through the rest of 2026. The Goldman Sachs Research team projects 1.4% GDP growth for full-year 2026, up from the underwhelming 1% seen in 2025, driven by recovering consumer spending and continued Bank of England rate cuts providing lift to the broader economy.

On inflation, the picture is brightening considerably. UK CPI fell to 3.0% in January 2026 — its lowest level since March 2025 — and the Bank of England’s own February 2026 forecast projects it to fall further to 2.1% by Q2 2026, landing close to the 2% target. The practical implication for everyday investors is significant: falling inflation reduces the “real” erosion of cash savings, but it does not reverse it. Money sitting in a current account is still losing purchasing power in real terms — which is precisely why SIP Investing in the UK offers such a powerful antidote. You can follow the latest Bank of England monetary policy thinking at bankofengland.co.uk.

The Bank of England is also on a confirmed rate-cutting path. Having already reduced the base rate to approximately 4.25–4.5%, it is expected to cut rates three more times in 2026 to reach a terminal rate of around 3%, per Goldman Sachs and Vanguard forecasts. Falling rates reduce returns on savings accounts and fixed-rate bonds — making the long-term growth potential of SIP Investing in the UK look increasingly attractive by comparison.

🎬 Watch: UK Economy 2026 – What Investors Need to Know

📱 The Digital Investment Revolution

The way Brits invest has been utterly transformed over the past five years, and in March 2026 that transformation continues to accelerate. According to the FCA’s Financial Lives Survey, over 5 million people in the UK now invest regularly through digital platforms — up from 4 million just two years ago. Auto-investing features, round-ups, and direct debit contributions make SIP Investing in the UK possible without any active effort after setup. You invest while you sleep, while you work, and while you enjoy your life.

Fractional shares — now available on platforms like Trading 212, Freetrade, and InvestEngine — mean that even premium global stocks are accessible to anyone with £1 to invest. The era of needing thousands of pounds to enter the market is firmly behind us. As Which? Money notes in its 2026 platform reviews, this democratisation of investing has been one of the most significant shifts in personal finance in a generation — and SIP Investing in the UK sits right at its centre.

📊 UK and International Fund Returns — March 2026 Reality Check

Before diving into returns, a critical note: these are historical averages and not guarantees of future performance. That said, the context matters enormously in 2026. The FTSE 100 has been one of the standout global indices over the past 12–18 months. In 2025, the FTSE 100 delivered a remarkable 21% annual gain — its best performance since 2009 — outperforming even the S&P 500’s 17% return, as reported by Forex.com’s market analysis. And in 2026, momentum has continued: by late February, the FTSE 100 had already hit a record high of 10,928, posting its eighth consecutive monthly gain — its strongest run since 2013, per Trading Economics.

Here is what that translates to in terms of broad fund categories relevant to SIP Investing in the UK:

FTSE 100 Index Funds have delivered a long-run historical average of approximately 7–9% annually (including dividends reinvested), and recent performance has surged well above that benchmark. UK Equity Funds have averaged 8–11% inclusive of dividend income. Global Tracker Funds, which give you diversified exposure beyond UK shores, have historically returned 9–12%, and continue to benefit from broad international growth. Income-focused funds, popular with retirees and cautious investors, typically target 5–7% through reliable dividend payments. For the latest independent comparison of these fund types, Hargreaves Lansdown’s fund research hub provides up-to-date data and ratings.

🎬 Watch: Best Index Funds UK 2026 – FTSE 100 vs Global Trackers Explained

🏆 Top Investment Platforms for SIP Investing in the UK — 2026 Edition

Choosing the right platform is one of the most impactful decisions you’ll make in your journey with SIP Investing in the UK, and the good news is that the UK market has some of the most competitive and consumer-friendly platforms in the world. Here is where each platform shines in 2026.

Vanguard UK remains the gold standard for cost-conscious, long-term investors. Its range of low-cost index funds makes it the natural first stop for anyone beginning SIP Investing in the UK on a budget. Hargreaves Lansdown, the UK’s largest investment platform with over 1.8 million clients, offers unmatched breadth and an exceptional research library — ideal if you want variety alongside guidance.

AJ Bell combines competitive pricing with a clean interface, particularly strong for those building a SIPP alongside their ISA. Trading 212 is the go-to for commission-free investing and fractional shares, making it perfect for those starting with smaller monthly amounts. And Interactive Investor operates on a flat-fee model that suits investors with larger portfolios, where percentage-based charges would otherwise eat deeply into returns.

All of these platforms are regulated by the Financial Conduct Authority, meaning your investments are protected under the Financial Services Compensation Scheme (FSCS) up to £85,000 — a crucial protection to understand before you begin. For an independently verified comparison of platform fees and features, MoneySavingExpert’s best stocks and shares ISA guide is updated regularly and free to access.

🎬 Watch: Best UK Investment Platforms 2026 – Compared & Ranked

💷 HMRC Tax Advantages for SIP Investing in the UK — 2025/26 Rules

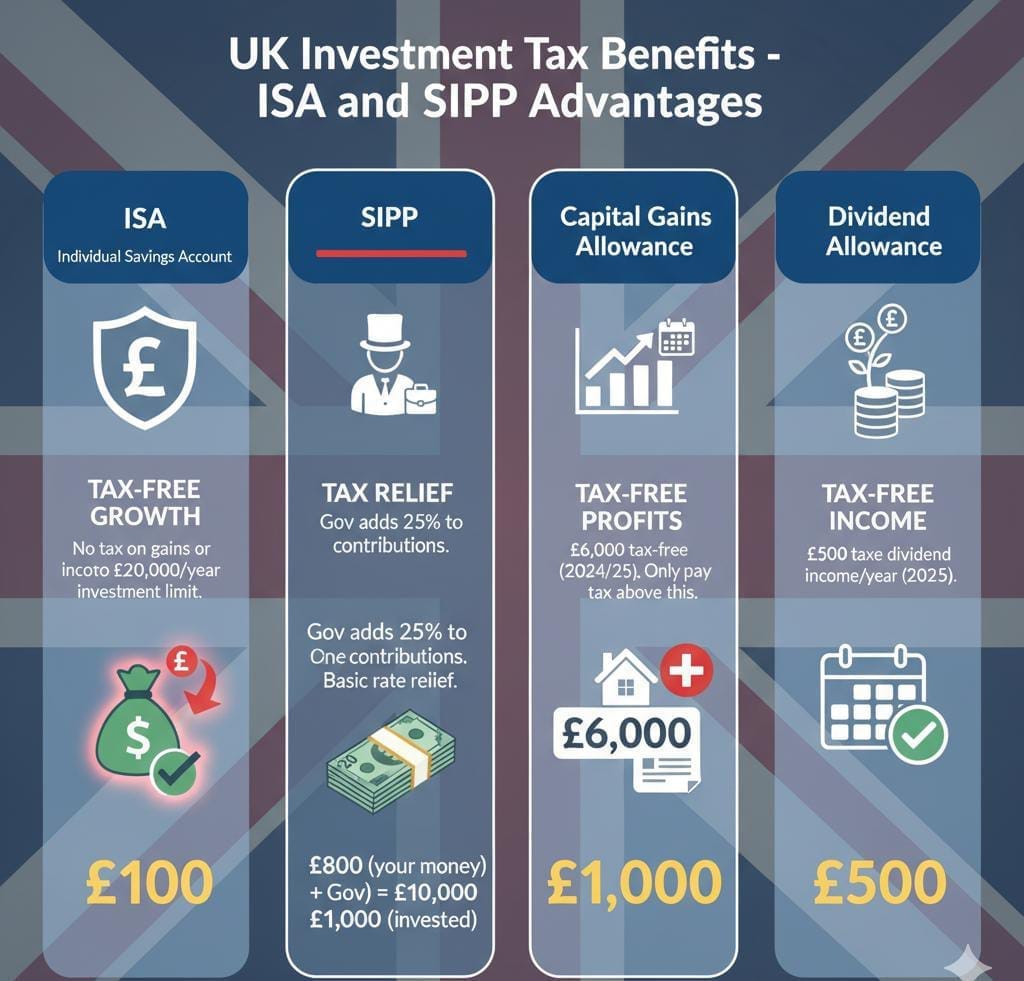

This is where SIP Investing in the UK becomes especially brilliant for British residents, because the UK tax system offers extraordinary advantages that most people do not fully exploit. For the 2025/26 tax year, your Stocks & Shares ISA allowance remains at £20,000 — meaning any gains, dividends, or interest earned inside that wrapper are completely free from UK Capital Gains Tax and Income Tax. You can confirm this directly at GOV.UK’s official ISA guide.

For pension-based SIP Investing in the UK through a SIPP, the annual pension allowance for 2025/26 is £60,000 (or 100% of your earnings, whichever is lower), as confirmed by HMRC’s pension allowance guidance. Contributions to a pension also attract tax relief at your marginal rate — meaning a basic-rate taxpayer effectively gets a 25% government top-up on every pound invested, while higher-rate taxpayers can reclaim up to 40% through their self-assessment tax return. This makes investing inside a pension one of the most tax-efficient strategies available to UK residents in 2026.

New from April 2026, the Consumer Composite Investments (CCI) regime introduced by the FCA requires all investment platforms to provide clearer, fairer product information to retail investors — so reading fund terms has never been easier or more straightforward. Full details are available via the FCA’s official CCI guidance.

- ISA Allowance: £20,000 annual tax-free investing

- SIPP Contributions: Tax relief on pension contributions

- Capital Gains Allowance: £3,000 tax-free gains annually

- Dividend Allowance: £500 tax-free dividend income

Official Source: HMRC Investment Guidance

🗓️ Step-by-Step SIP Investing in the UK — 2026 Starting Guide

One of the most common reasons people delay beginning their investment journey is the mistaken belief that it is complicated. It is not. SIP Investing in the UK follows a clear, logical sequence, and once you understand the structure, you will wonder why you ever waited. Here is your complete, up-to-date guide for March 2026 — written to take you from zero to automatic investor in just one week.

🎬 Watch First: How to Start Investing in the UK — Complete Beginner’s Guide 2024

Step 1: Choose Your Investment Wrapper

Think of an investment wrapper as the tax-friendly container that holds your investments. Choosing the right one is arguably the most impactful decision you will make in your SIP Investing in the UK journey, because the wrapper determines how much of your returns you actually keep.

The Stocks and Shares ISA is the natural first choice for most UK investors in 2026. Every pound of growth, dividend, and interest earned inside it is completely invisible to HMRC — no Capital Gains Tax, no Income Tax, no reporting required. With the Capital Gains Tax allowance now slashed to just £3,000 and dividend tax rates rising from April 2026, investing outside an ISA has become highly inefficient. Fincart You can confirm the current rules at GOV.UK’s official ISA guide. Critically, the 2026/27 tax year is your most important window yet — the full £20,000 allowance is available now, but the cash ISA cap drops to £12,000 for under-65s in April 2027 Fincart, making this the year to act decisively.

The Self-Invested Personal Pension (SIPP) is the preferred wrapper for those focused on retirement wealth. Every contribution you make attracts government tax relief at your marginal rate — meaning a basic-rate taxpayer effectively gets a 25% top-up from the government on every pound they invest. The annual pension allowance for 2025/26 remains at £60,000, as confirmed by HMRC.

The trade-off is that you cannot access your pension pot until age 57 (rising to 57 from 2028), so a SIPP works best as a long-term complement to your ISA rather than a replacement. The General Investment Account (GIA) is available for those who wish to invest beyond their £20,000 ISA limit, though gains here are subject to the reduced CGT allowance, which underscores why maxing your ISA first is always the priority in any SIP Investing in the UK strategy.

Step 2: Select Your Platform

Choosing the right platform is like choosing the right bank — it needs to suit your style, your budget, and your goals. The good news is that the UK market in 2026 has some of the most competitive, transparent, and consumer-friendly investment platforms in the world. All of the platforms listed here are regulated by the Financial Conduct Authority, and your investments are protected under the Financial Services Compensation Scheme (FSCS) up to £85,000 in the event a platform fails — though it is important to understand that FSCS protection covers platform failure, not market losses.

Vanguard UK remains the gold standard for cost-conscious, long-term index investors. Vanguard’s stocks and shares ISA is a great choice for investors who value simplicity and low overhead Western Business, making it the natural home for anyone beginning SIP Investing in the UK on a budget. Hargreaves Lansdown, the UK’s largest platform with over 1.8 million clients, offers unmatched breadth of funds and an exceptional research library. AJ Bell provides competitive pricing with excellent regular-investing features, particularly well-suited for those building both an ISA and a SIPP simultaneously.

Trading 212 is the go-to platform for commission-free investing and fractional shares, perfect for those starting with smaller monthly amounts. InvestEngine operates a zero-fee DIY model — no annual platform charges, no dealing commissions — making it arguably the most economical vehicle for those building long-term wealth through index tracking Western Business. And Interactive Investor suits larger portfolios with its flat-fee model, which becomes dramatically more cost-effective once your portfolio grows past approximately £50,000. For an independently verified, up-to-date comparison of all major platforms, MoneySavingExpert’s Stocks & Shares ISA guide is the most trusted free resource available to UK investors in 2026.

🎬 Watch: Best UK Investment Platforms 2026 — Ranked & Compared

Step 3: Pick Your First Investments — 2026 Strategy

For the vast majority of people beginning SIP Investing in the UK, the single best starting point is a broad, low-cost index fund — either a FTSE All-Share tracker or a global equity tracker. These give you instant, automatic diversification across hundreds or thousands of companies, professional index management built in, and historically proven long-term returns — all for a fraction of the cost of actively managed funds.

Three outstanding starter choices in 2026 are the Vanguard FTSE UK All Share Index Unit Trust, the iShares Core FTSE 100 UCITS ETF, and the HSBC FTSE All-Share Index Fund — all widely available across the major UK platforms and consistently among the most cost-effective options in their category. The average annual return on a stocks and shares ISA over the past 10 years has been 9.64%, compared to just 1.2% for cash ISAs Aviva — a striking illustration of why long-term investing beats saving for those with a horizon of five or more years.

Step 4: Set Up Automatic Investments

This is the step that transforms SIP Investing in the UK from a good idea into a working financial machine. Set up a direct debit from your UK bank account to your chosen platform, starting with as little as £50 per month. Select monthly as your investment frequency — it aligns with most UK pay cycles and keeps your pound cost averaging consistent.

\ Then enable auto-invest, which ensures your contributions are automatically deployed into your chosen fund the moment they land in your account. The beauty of this approach is that once it is set up, it requires almost no active management. You invest automatically whether markets are rising or falling — and as Wealthify explains, investors who automate their contributions are far less likely to panic-sell during market dips, which is where most retail investors historically lose the most money.

Step 5: Stay the Course

The fifth step is arguably the hardest — because it requires you to do almost nothing. Review your portfolio once a year, ideally at the start of each new tax year in April. Resist the temptation to check prices daily, as short-term volatility is entirely normal and largely irrelevant to a long-term systematic investor. \

Never pause your automatic investments during market downturns — in fact, a falling market means your fixed monthly contribution buys more units at lower prices, which is precisely when pound cost averaging works best in your favour. And wherever possible, increase your contributions in line with salary increments — maintaining your lifestyle while letting a larger proportion of each pay rise work for you automatically. As the FCA’s consumer investment principles consistently emphasise, patience and consistency are the defining characteristics of successful long-term investors.

🧠 Advanced 2026 Strategies for UK Investors

Once you have mastered the basics of SIP Investing in the UK, there are several intermediate-level strategies worth layering in as your confidence and portfolio grow.

The Salary Increase Strategy is elegantly simple: every time you receive a pay rise, increase your automatic investment by the same percentage. This means your lifestyle does not expand to swallow the extra income, and your wealth-building accelerates quietly in the background. Over a decade of career progression, this habit alone can dramatically compound your final portfolio value.

The Three-Bucket British Portfolio is a popular framework that allocates your investments across three distinct areas: approximately 40% in UK equities (benefiting from FTSE dividend income and home-market familiarity), 40% in global equities (providing international diversification and exposure to faster-growing global economies), and 20% in bonds and gilts (providing a capital-preservation cushion during market turbulence). This allocation is a widely recommended starting point for intermediate UK investors, though the precise split should reflect your individual risk tolerance, time horizon, and retirement goals. For a more personalised assessment, Vanguard UK’s investor questionnaire is an excellent free tool.

Pension Optimisation through salary sacrifice is another strategy that deserves attention in 2026. By routing additional pension contributions through your employer’s payroll as salary sacrifice, you avoid National Insurance contributions on those amounts — effectively giving yourself a further tax saving on top of the income tax relief. Many employers will also match additional voluntary contributions up to a certain percentage, which is quite simply free money that should never be left on the table. Full guidance is available at HMRC’s pension contributions page.

🎬 Watch: Advanced UK Investing Strategies — ISA, SIPP & Salary Sacrifice Explained

⚠️ Common 2026 SIP Investing in the UK Mistakes to Avoid

The FCA’s Consumer Duty regulations, now fully embedded across the UK investment industry since 2023 and actively enforced in 2026, have done a great deal to improve platform transparency and protect retail investors. But even the best regulatory framework cannot protect you from your own behavioural tendencies — and these are where most investment journeys go wrong.

Market timing attempts — waiting for the “right” moment to invest — are the single most common and damaging mistake. Even professional fund managers consistently fail to time markets accurately. For a systematic investor, the right moment is always now, because time in the market beats time at the market over the long run. Ignoring platform fees is a subtler error but equally costly. A difference of just 0.5% in annual platform charges compounds into tens of thousands of pounds over a 30-year investment horizon — which is why comparing fees before choosing a platform is so important, and why Which? Money’s platform comparison tool is worth consulting.

Overcomplicating your portfolio by holding too many overlapping funds creates confusion, false diversification, and unnecessary costs without meaningfully reducing risk. Emotional decision-making — buying during market highs driven by excitement, and selling during market lows driven by fear — is the pattern that transfers wealth from impatient investors to patient ones. And neglecting tax wrappers by investing in a General Investment Account before maximising your ISA and pension allowances is leaving free government money on the table. A higher-rate taxpayer investing £20,000 keeps approximately £4,843 more over a decade simply by using an ISA Citisoft — a compelling illustration of just how much wrapper selection matters in any SIP Investing in the UK plan.

❓ Frequently Asked Questions — 2026 British Edition

Can I genuinely start with just £50 monthly? Absolutely. Most major UK platforms — including Vanguard, AJ Bell, and Hargreaves Lansdown — accept a £50 monthly minimum, and some, including Trading 212 and InvestEngine, accept even less through fractional share investing. The important thing is not the size of the initial contribution but the consistency of the habit.

Are these platforms properly regulated and safe? Yes. Every platform listed in this guide is regulated by the Financial Conduct Authority and covered by the FSCS up to £85,000 per person, per firm. You can verify the regulatory status of any UK investment platform using the FCA’s Financial Services Register.

What about tax on my investment returns? Within a Stocks & Shares ISA, all returns — capital growth, dividends, and interest — are completely tax-free, with no reporting to HMRC required. Outside an ISA, the CGT allowance is now just £3,000 for 2025/26, which is precisely why ISA-first investing is so critical in SIP Investing in the UK today.

Should I focus on my pension or invest in an ISA? Both serve important and complementary roles. Your pension offers superior tax relief on contributions and employer matching, making it the most efficient vehicle for retirement savings. Your ISA offers complete flexibility — no minimum age for access, no restrictions on withdrawals — making it ideal for medium-term goals like a home purchase, school fees, or early retirement. An optimal UK strategy typically involves contributing enough to your pension to capture any employer match, then directing surplus savings into an ISA.

📊 Industry Growth Metrics — UK 2026 Update

The data on UK retail investing is genuinely encouraging. A quarter of UK adults — 26% — now have a stocks and shares ISA as of 2026, and an additional 17% of Brits who don’t currently have one intend to open one this year. Aviva 4.1 million people subscribed to a stocks and shares ISA in the 2023/24 tax year, up from 3.8 million in 2022/23 Aviva — a trend that has continued into 2026.

In the early weeks of 2026, private investors have continued piling spare cash into UK shares, with January characterised by notable diversification across sectors Womble Bond Dickinson, according to Interactive Investor. Youth participation has grown markedly too, with 40% of new ISA investors under 35 — a generation that has embraced digital platforms and understands instinctively that SIP Investing in the UK is how long-term financial independence is built. Digital platform growth continues at approximately 30% annually, driven by mobile-first apps, auto-investing tools, and fractional shares that lower the barrier to entry to almost zero.

📅 Your 7-Day British Investment Launch Plan

Starting SIP Investing in the UK does not need to take weeks of research. Here is a concrete, day-by-day plan to get you from reading this article to having your first automatic investment running within one week.

On Day 1, use the FCA’s compound interest calculator to model your financial goals — how much you want to accumulate, over what time horizon, and at what monthly contribution level. On Day 2, research and shortlist your preferred platform using MoneySavingExpert and Which? as independent guides. On Day 3, gather the documents you will need:

your National Insurance number, proof of address, and bank account details. On Day 4, open your Stocks and Shares ISA online — most platforms complete the process in under 15 minutes. On Day 5, set up your first £50 (or more) automatic investment via direct debit, selecting your chosen index fund or global tracker. On Day 6, schedule a calendar reminder for an annual portfolio review —

same time next year. And on Day 7, bookmark MoneyHelper and the FCA’s consumer resources page to continue your financial education at your own pace.

👾 Special Section: Young British Investors

For students and young professionals, SIP Investing in the UK offers a compounding advantage that no amount of financial sophistication in later life can fully replicate: time. Beginning at 22 rather than 32 can, in practical terms, more than double your final retirement pot from the same monthly contributions — purely because of the extra decade of compound growth.

The Lifetime ISA (LISA) deserves specific mention for under-40s: you can contribute up to £4,000 per year and receive an automatic 25% government bonus — up to £1,000 of free money annually — which can be used for a first home purchase or retirement. Full details are at GOV.UK’s Lifetime ISA guide. Robo-advisors such as Moneyfarm, Nutmeg, and Wealthify offer fully automated portfolio management, making them an ideal gateway into SIP Investing in the UK for those who prefer a hands-off approach while they build their financial knowledge. And the golden rule for young investors in 2026 is simply this: start small, start now, and let decades of compounding do the extraordinary work that feels impossible in the short term.

🏁 Final Motivation: Build Your British Financial Future

As the esteemed British fund manager Terry Smith has observed: the stock market rewards those who are patient and punishes those who are not. Your £50 automatic investment today is not just a financial transaction — it is a declaration of patience, a commitment to your future self, and a recognition that building lasting wealth is a marathon, not a sprint. In the sophisticated, well-regulated environment of UK financial markets in 2026 — with strong FCA Consumer Duty protections, exceptional ISA tax advantages, access to global companies through fractional shares, and an annual pension allowance of £60,000 — the conditions for SIP Investing in the UK have arguably never been more favourable for everyday investors.

The average annual return on a stocks and shares ISA over the past decade has been 9.64% Aviva — more than seven times the return on a cash ISA over the same period. The statistics, the regulation, the technology, and the tax advantages all point in the same direction. Over 4 million Britons are already systematically securing their financial futures. You now have everything you need to join them. Do not overanalyse. Do not wait for someday. Open your ISA, set your direct debit, and let SIP Investing in the UK begin working for you — starting today. Cheers! 🇬🇧

for more info visit Lumechronos

⚠️ Disclaimer: Investing involves risk, including the possible loss of capital. Past performance does not guarantee future results. This content is for educational purposes only and does not constitute regulated financial advice. Tax treatment depends on individual circumstances and may change. Always consider your personal situation and consult an FCA-authorised financial adviser before making investment decisions. FSCS protection of up to £85,000 applies per person, per regulated firm, covering platform failure — not market losses.

Leave a Reply