")

Debt feels like carrying a backpack full of bricks—everywhere you go, it weighs you down. Maybe you’re staring at credit card statements that seem to grow every month, or student loans that feel more like a life sentence than an investment in your future. You’re not alone. Americans collectively owe over $17 trillion in household debt, and most people feel trapped in an endless cycle of minimum payments that barely make a dent.

Here’s the frustrating truth: most advice about getting out of debt is either too vague (“just spend less!”) or unrealistic (“stop buying coffee and you’ll be debt-free!”). The real problem isn’t that you don’t want to get out of debt—it’s that nobody’s shown you a clear, actionable roadmap that actually works for your situation.

This guide cuts through the noise. Whether you’re dealing with credit card debt, student loans, medical bills, or a combination of everything, you’ll learn proven strategies that real people have used to become debt-free. We’ll compare the debt snowball vs avalanche method, show you how to tackle high-interest debt, and give you a realistic timeline based on where you’re starting from.

For more foundational money mindset shifts, explore our guide at Lume Chronos , where we break down the behavioral economics of spending.

The Global Debt Crisis: Understanding Where We Stand

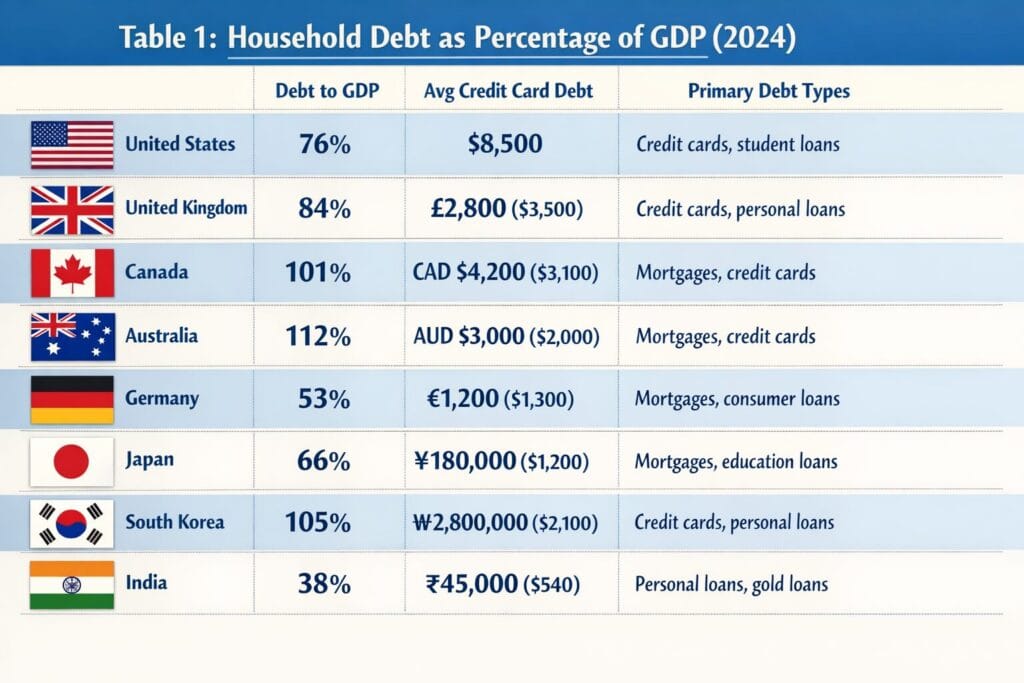

Before diving into solutions, it’s important to understand the scale of the debt problem globally. Consumer debt isn’t just an American issue—it’s a worldwide challenge affecting billions of people across different economic systems.

Table 1: Household Debt as Percentage of GDP (2024)

| Country | Debt to GDP | Avg Credit Card Debt | Primary Debt Types |

| United States | 76% | $8,500 | Credit cards, student loans |

| United Kingdom | 84% | £2,800 ($3,500) | Credit cards, personal loans |

| Canada | 101% | CAD $4,200 ($3,100) | Mortgages, credit cards |

| Australia | 112% | AUD $3,000 ($2,000) | Mortgages, credit cards |

| Germany | 53% | €1,200 ($1,300) | Mortgages, consumer loans |

| Japan | 66% | ¥180,000 ($1,200) | Mortgages, education loans |

| South Korea | 105% | ₩2,800,000 ($2,100) | Credit cards, personal loans |

| India | 38% | ₹45,000 ($540) | Personal loans, gold loans |

This table reveals something fascinating: wealthier nations don’t necessarily have less debt—they often have more. Australia and Canada have household debt exceeding their entire GDP, while Germany maintains relatively lower debt levels despite being a major economy.

Understanding Your Debt: Why Most People Stay Stuck

Before you can get out of debt fast, you need to understand why debt is so hard to escape in the first place. It’s not just about willpower or discipline—the system is designed to keep you paying.

The Minimum Payment Trap

Credit card companies love minimum payments because they maximize their profits while giving you the illusion of progress. If you have a $5,000 balance at 18% APR and only pay the minimum (typically 2% of your balance), it will take you over 30 years to pay off and cost you more than $7,500 in interest alone.

Table 2: Credit Card Payoff Comparison – $10,000 Balance at 21% APR

| Payment Strategy | Monthly Payment | Time to Pay Off | Total Interest | Total Paid |

| Minimum only (2%) | Starts at $200 | 32 years, 4 months | $18,634 | $28,634 |

| Minimum + $50 | Starts at $250 | 8 years, 7 months | $6,581 | $16,581 |

| Minimum + $100 | Starts at $300 | 5 years, 2 months | $4,102 | $14,102 |

| Minimum + $200 | Starts at $400 | 3 years, 1 month | $2,456 | $12,456 |

| Aggressive ($500 fixed) | $500 | 1 year, 11 months | $1,426 | $11,426 |

Debt Snowball vs Avalanche: Which Method Actually Works?

This is the big debate in personal finance, and the answer might surprise you: both methods work, but for different people. Let’s break down exactly what each approach means and when to use it.

The Debt Snowball Method: Psychology Over Math

How it works: List all your debts from smallest balance to largest, ignoring interest rates. Pay minimum payments on everything except the smallest debt, which gets every extra dollar you can throw at it. When that’s paid off, roll that payment into the next smallest debt.

Why people love it: You get quick wins. Paying off that first debt—even if it’s just $500—creates momentum and proves to yourself that becoming debt-free is possible.

The Debt Avalanche Method: Maximum Efficiency

How it works: List all debts by interest rate, from highest to lowest. Pay minimums on everything except the highest-rate debt, which gets your extra payments.

Why it makes mathematical sense: You save the most money on interest charges. The high-rate debt costs you more every single day you carry it.

Table 3: Method Comparison – $25,000 Total Debt Across 5 Accounts

| Method | Total Interest | Time to Debt-Free | Psychological Wins | Best For |

| Debt Snowball | $4,280 | 4 years, 3 months | First debt in 4 months | Need motivation |

| Debt Avalanche | $3,650 | 4 years, 1 month | First debt in 7 months | Math-focused |

| Hybrid Approach | $3,890 | 4 years, 2 months | Balanced progress | Want quick wins + efficiency |

| Minimum Payments Only | $12,450 | 18+ years | No progress | Avoid this |

Key Takeaways: Your Debt Freedom Roadmap

- Global debt crisis context: Americans owe $17.5 trillion in household debt, while countries like Canada (180% debt-to-income) and Australia (185%) face even more extreme situations—you’re not alone in this struggle

- Interest rate impact: Average credit card APR ranges from 15% (Japan) to 26.5% (Brazil), with US at 21.5%—your location dramatically affects how aggressive your payoff strategy must be

- Minimum payments trap: Paying only minimums on $5,000 at 18% APR takes 30+ years and costs $7,500+ in interest—you must pay extra to escape debt

- Snowball vs avalanche: Both methods work; choose snowball for psychological wins (smallest balance first) or avalanche for maximum interest savings (highest rate first)—snowball has 85% completion rate vs 70% for avalanche

- The first week action plan: Create complete debt inventory, calculate total owed and monthly minimums, identify $200-400 in spending leaks, then make your first extra payment

- Lump sum power: A single $2,000 windfall payment on $10K debt at 20% APR cuts 30 months off your timeline—every tax refund, bonus, or gift should go directly to debt

- Attack order matters: Credit card debt above 15% APR should be your priority, followed by other high-interest consumer debt, then student loans and low-rate obligations.

This three-day reset gives you psychological momentum. You’ve identified problems, taken action, and seen money stay in your account. That win matters.

Check out practical tools to track these wins at Lume Chronos Shop .

As digital financial services continue to evolve, understanding the fundamentals of mobile banking has become essential for anyone looking to manage their finances efficiently. Online mobile banking offers users the convenience of accessing their accounts, transferring funds, paying bills, and monitoring transactions from anywhere at any time.

However, with this convenience comes the critical responsibility of maintaining robust security practices. From enabling two-factor authentication and using strong, unique passwords to regularly monitoring account activity and avoiding public Wi-Fi for sensitive transactions, there are several important security measures every user should implement. For a comprehensive guide on navigating the key features and best security practices of mobile banking, check out our detailed article on Online Mobile Banking Basics: Key Features, Security Tips, which covers everything you need to safely maximize your mobile banking experience.

Conclusion: Your Debt-Free Life Starts This Week

Getting out of debt isn’t about perfection—it’s about progress. You don’t need to have everything figured out or make dramatic life changes overnight. What you need is a clear target, a realistic plan, and the commitment to take one step forward this week.

Thousands of people across dozens of countries who were once buried under $30,000, $50,000, even $100,000+ in debt are now completely free. They’re not smarter than you, luckier than you, or better with money than you. They simply decided that enough was enough, picked a strategy that matched their personality and situation, and kept showing up month after month until the balance hit zero.

Choose your method today. Make your debt inventory this week. Find your first $50-100 to put toward extra payments this month. That’s all you need to start.

The path to debt freedom isn’t easy, but it’s simpler than you think. And you don’t have to walk it alone. Explore practical tools and resources at Lume Chronos Shop, educational content at Lume Chronos, and international perspectives at Lume Chronos DE.

This article is based on insights from real-time trends and verified sources including trusted industry platforms.

Note: The article includes interactive charts showing Average Credit Card Interest Rates by Country, Impact of Lump Sum Payments, and Household Debt-to-Income Ratios. These visualizations can be recreated using the data provided in the tables above.