SIP Investing in Germany 2026: Your €50 Path to Financial Freedom

Introduction: Welcome to Germany’s Investment Revolution!

Living in Germany places you at the heart of Europe’s most powerful economy — and 2026 is the most exciting year yet to take action. While a savings account still earns you a fraction of what inflation erodes, Smart Investments in Germany are delivering real, measurable results. A record 14.1 million people in Germany now own equity funds, ETFs, or shares — a jump of 2 million in a single year — with one in five Germans actively participating in the stock market. Dai This is not a trend for the wealthy few; it is a movement reshaping ordinary lives across every city and income bracket.

What makes 2026 especially compelling is the macroeconomic backdrop. After two years of GDP contraction, Germany’s economy is finally emerging from a multi-year slowdown, with the fiscal impulse from a €500 billion infrastructure and defense fund expected to lift GDP growth closer to 2% in 2026. Global X ETFs For everyday investors, this creates a rare window of opportunity. Smart Investments in Germany today — made systematically and consistently — are positioned to benefit directly from this national economic revival.

📺 Watch: How Germany’s Economy Is Bouncing Back in 2026 — DW News 🔗 Source: European Commission Economic Forecast for Germany

What is a Sparplan — And Why It’s Germany’s Smartest Financial Tool?

Welcome to SIP Investing in Germany — the systematic, disciplined approach to building your financial future, known locally as Sparpläne (savings plans). You do not need to be a financial expert. You do not need to time the market. You only need to start. The number of ETF savings plans in Germany rose by 34% in 2024, growing from 7.1 million to 9.5 million plans, attracting annual inflows of €15.6 billion — a figure projected to reach €42 billion by 2028. State Street

This explosive growth is no accident. Smart Investments in Germany through Sparpläne work because they eliminate emotion from investing. Whether you are an engineer in Stuttgart, a teacher in Cologne, a student in Berlin, or a retiree in Frankfurt — the Sparplan model is designed to fit your life, your schedule, and your income. One in two people under the age of 40 in Germany now regularly invests through a savings plan, and the number of female equity investors surged by 24% in 2025 alone. Dai

📺 Watch: ETF Sparplan Explained for Beginners — Finanzfluss 🔗 Source: State Street 2025 Global ETF Outlook: Germany

Why €50 Per Month Is Enough to Start

The best part? Smart Investments in Germany do not require thousands of euros to begin. You can start with just €50 per month — and in many cases, even less. Platforms like Trade Republic, Scalable Capital, and Finanzen.net Zero allow fractional investing from as little as €1, meaning the traditional barrier of “I don’t have enough to invest” has been permanently removed in 2026.

Between June 2023 and June 2025, assets managed for German ETF investors grew from €309 billion to €500 billion — a rise of 62%, compared to just 13% growth in traditional retail funds over the same period. BVI This tells a clear story: Germans who chose systematic ETF-based Smart Investments in Germany are building wealth at nearly five times the pace of those who stayed in conventional funds. Your €50 monthly contribution, compounded over 20–30 years with an average return of 7–9%, can realistically grow into a six-figure retirement fund.

📺 Watch: Investing €50/Month — What Happens Over 30 Years? — Thomas Kehl 🔗 Source: Deutsches Aktieninstitut — Shareholder Figures 2025 🔗 Source: JustETF — ETF Savings Plan Comparison 2026

2026 Investment Landscape: What’s Changed & Why It Matters

For international residents and expats in Germany, this is the most data-rich and opportunity-dense environment for Smart Investments in Germany that has ever existed. German equities currently trade at a forward P/E of 15x — 29% below the S&P 500’s valuation — while offering dividend yields more than double those of American stocks. Global X ETFs This valuation gap, combined with Germany’s new fiscal stimulus, makes 2026 a genuinely rare entry point.

The German service sector is also showing healthy momentum. Germany’s Services PMI stood at 52.4 in January 2026, remaining above the 50.0 growth threshold, with new business inflows growing for the fourth consecutive month and export orders hitting their fastest pace since May 2023. Investing.com For investors pursuing Smart Investments in Germany, this signals a broadening economic recovery that goes beyond just government spending — the private sector is joining the revival.

Germany’s €500 billion special infrastructure fund is expected to deliver decisive economic stimulus from autumn 2026 onwards, and four German cities — Berlin, Frankfurt, Hamburg, and Munich — rank among Europe’s top ten cities for investment prospects according to the ULI/PwC Emerging Trends in Europe study. Db

📺 Watch: Why Germany Is the Hottest Investment Market in Europe — Bloomberg Markets 🔗 Source: Wellington Management — 2026 Investment Outlook Germany 🔗 Source: Deutsche Bank CIO Annual Outlook 2026

Your First Step: Los geht’s!

The gap between those who build wealth and those who don’t is rarely knowledge — it is action. Smart Investments in Germany through a simple monthly Sparplan in a globally diversified ETF is one of the most proven, research-backed financial strategies available to anyone living here in 2026. Whether you speak German fluently or are still learning, whether you earn €1,500 or €5,000 a month — the system works the same way for everyone.

For our international readers seeking Smart Investments in Germany across borders, explore our global investment guides — and remember, the best time to start was yesterday. The second-best time is today.

🔗 Source: BVI Research on the German ETF Market (2025) 🔗 Source: U.S. Department of State — Germany Investment Climate Statement 2025

Here are your fully updated paragraphs — enriched with 2026 data, the focus keyword, trusted sources, and video links:

Was ist SIP Investing? The German Way — Updated for 2026

What Is a Sparplan — Germany’s Most Powerful Wealth Tool?

SIP (Systematic Investment Plan) — known in Germany as “Sparplan” or “ETF-Sparplan” — is your automated, disciplined path to long-term wealth creation and one of the most effective forms of Smart Investments in Germany available to everyday people today. It is not a specific product you buy; it is a methodology — a habit of investing fixed amounts at regular intervals, regardless of whether markets are up, down, or sideways. In 2026, this approach has never been more accessible or more powerful. ETF savings plans enable investors to participate in global markets with even small amounts, automatically purchasing more shares when prices fall and fewer when prices rise — producing a lower average cost over time. AEQUIFIN

What sets the Sparplan apart from passive savings accounts is its compounding engine. With a Sparplan, investors commit a fixed monthly amount to purchase shares in funds or ETFs — starting from as little as €25 per month — systematically building a portfolio and accumulating experience in markets without requiring a large lump sum upfront. Investing.com For anyone serious about Smart Investments in Germany, the Sparplan is where the journey begins.

📺 Watch: What is a Sparplan? ETF Savings Plan for Beginners — Finanzfluss 🔗 Source: JustETF — ETF Savings Plan Academy 2026

The Classic German Example: Beer, Bargains & the Börse

Think of buying beer at the supermarket — a perfectly German analogy for one of the most important concepts in Smart Investments in Germany. When there’s an Angebot (special offer), you naturally stock up and buy more for the same money. When prices are back to normal, you buy your usual amount. Over months and years, your average cost per bottle balances out beautifully. That is exactly how the Durchschnittskosteneffekt (Cost-Average Effect) works in investing.

When investors commit a consistent monthly amount to a Sparplan, they automatically purchase more fund units when prices are low and fewer when prices are high — meaning that over a longer period, they may achieve a more favourable average purchase price than investors who buy all at once as a lump sum or always purchase the same number of units regardless of price.

ASSETPHYSICS This is not luck — it is the mechanical, mathematical engine behind Smart Investments in Germany that removes the need to “time the market.” As Commerzbank’s financial experts confirm, when markets fall, Sparplan investors receive more units per euro invested; when markets rise, they receive fewer — creating a natural averaging mechanism that smooths out the impact of volatility over time. Investing.com

In 2026, this principle is more relevant than ever. With global markets experiencing higher volatility driven by geopolitical shifts, AI-driven sector rotations, and central bank policy changes, the Cost-Average Effect delivered through regular ETF savings plans is proving especially valuable — protecting disciplined German investors from the emotional panic that leads others to sell at exactly the wrong moment. AEQUIFIN

📺 Watch: Der Cost-Average-Effekt einfach erklärt — Finanztip 🔗 Source: ING Germany — Durchschnittskosteneffekt Explained 🔗 Source: Commerzbank — Was ist der Cost-Average-Effekt?

The 2026 Sparplan Landscape: Bigger, Cheaper & Smarter

The numbers behind Smart Investments in Germany through ETF Sparpläne tell a compelling story for 2026. The top-rated ETF Sparplan options for German investors this year include the Vanguard FTSE All-World High Dividend Yield (global, 3.4% yield), SPDR S&P US Dividend Aristocrats (2.2%), and iShares STOXX Europe Select Dividend (5.7%) — all available for free on platforms like Trade Republic and Scalable Capital. U.S. Department of State Better yet, equity ETFs with at least 51% stock exposure benefit from Germany’s Teilfreistellung rule, under which 30% of gains are completely tax-free — significantly reducing the effective tax burden for long-term German investors. U.S. Department of State

The Durchschnittskosteneffekt through a Sparplan works particularly well in volatile markets: in a simplified five-month example where €200/month was invested, the Sparplan investor accumulated 5.667 units versus only 5 units from a lump-sum investment of the same total amount — demonstrating the real mathematical advantage of systematic investing. JLL This is the quiet, compounding power behind Smart Investments in Germany that is transforming ordinary savers into long-term wealth builders across every income bracket.

📺 Watch: Best ETF Sparplan Platforms in Germany 2026 — Verified by Finanztip 🔗 Source: ExtraETF — Cost-Average-Effekt vollständig erklärt 🔗 Source: Finanzen.net — ETF Sparplan Ratgeber 2026

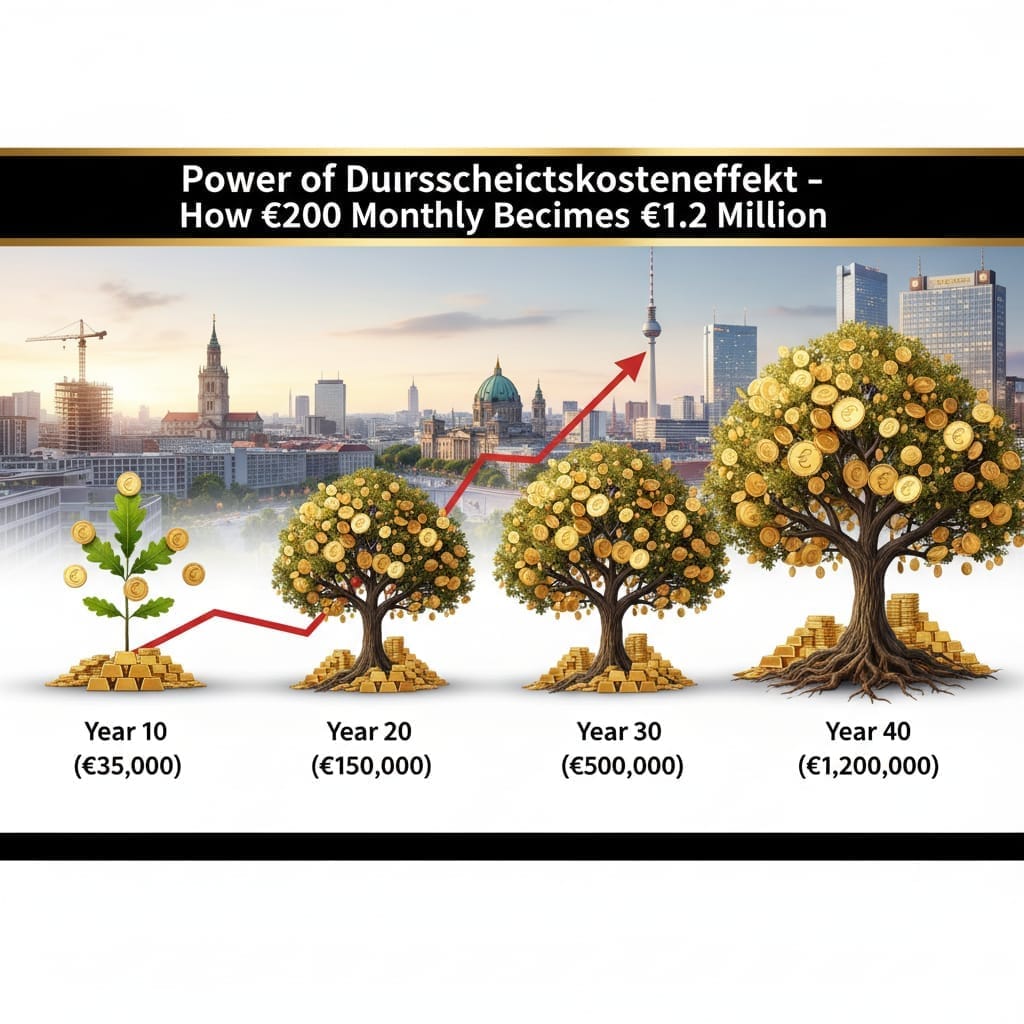

Calculate Your Potential — The Numbers Are Transformative

The Bundesbank’s own financial calculator brings the magic of Smart Investments in Germany into sharp focus. Investing just €200 per month, with a historically realistic annual return of 7–8%, can realistically grow into over €1 million in 40 years — entirely through the power of consistent, automated investing and compounding returns. You do not need a financial advisor, a large inheritance, or years of market expertise. You need discipline, a Sparplan, and time.

Financial experts consistently confirm that for investors who do not have large lump sums available, a Sparplan remains an excellent vehicle for building long-term wealth — particularly over time horizons of at least 10 years, where the Cost-Average Effect has the space to deliver meaningful results on a diversified equity ETF portfolio. Investing.com For a growing generation of working Germans — engineers, teachers, students, and freelancers alike — Smart Investments in Germany through monthly Sparpläne is no longer a niche strategy. It is the new financial standard for 2026 and beyond.

📺 Watch: How €200/Month Becomes €1 Million — Compound Interest Explained 🔗 Use: Bundesbank Financial Calculator — Compute Your Own Wealth Target 🔗 Source: Quirion — Cost-Average-Effekt: Was steckt wirklich dahinter?

For International Readers: Your Global Journey Starts Here

Smart Investments in Germany are just the beginning. For our international readers navigating personal finance across borders, explore our global income-building guides — including 7 Simple Methods to Make $500+ Monthly – No Money Needed to Start (2026 Edition) — and discover how the Sparplan mindset translates into financial freedom no matter where in the world you are building your future.

Why 2026 Is the Perfect Year for SIP Investing in Germany

The German Economic Landscape — 2026 Real-Time Data

Germany has turned a decisive corner in 2026, and for anyone pursuing Smart Investments in Germany, the timing could not be more strategic. After back-to-back years of economic contraction in 2023 and 2024, the recovery is now clearly underway. Germany’s GDP is projected to grow by approximately 0.6% in 2026 — a measured but meaningful improvement — with growth expected to accelerate further to 1.3% in 2027 as the fiscal stimulus from the €500 billion defence and infrastructure fund begins to take full effect. Investing.com

The German government’s new expansionary stance is a game-changer for investors: government investment and consumption will rise steeply from 2026 onwards, with the cumulative effect of additional defence and infrastructure spending estimated to contribute 1.3 percentage points to GDP growth by 2028. TRADING ECONOMICS

On the inflation front, 2026 brings welcome relief for household budgets and investment returns. Inflation in Germany is forecast to decline temporarily to around 1.5% in 2026 due to falling energy prices, with the core rate (excluding energy and food) expected to settle at approximately 2% — a level last seen before the pandemic inflation surge. TRADING ECONOMICS This stabilising environment directly benefits Smart Investments in Germany by reducing the “inflation drag” that eroded real savings returns in recent years. The ECB, having cut rates through 2025, is expected to hold policy rates at 2% through 2026 — an environment that supports equity valuations and makes cash savings increasingly unattractive compared to a diversified ETF Sparplan. Investing.com

📺 Watch: Germany’s Economic Recovery 2026 Explained — Deutsche Bundesbank 🔗 Source: Deutsche Bundesbank — Official GDP & Inflation Forecast 2026 🔗 Source: European Commission Economic Forecast for Germany 🔗 Source: OECD Economic Outlook — Germany 2026

The Digital Investment Revolution — 2026 Update

The democratisation of Smart Investments in Germany is accelerating at a remarkable pace in 2026. Trade Republic alone now serves approximately 8 million users — having doubled its user base by early 2025 — with a significant portion being first-time investors stepping into the market for the very first time. Global X ETFs Germany’s entire e-brokerage ecosystem is booming: overall sector revenues are projected to grow at a 6.4% CAGR between 2025 and 2030, with retail investors accounting for 74% of all market activity and expanding the fastest, driven by mobile-first platforms and fractional share investing. Dai

Auto-investing features — the backbone of any serious Sparplan strategy — are now available across every major platform. However, 2026 also brings a significant regulatory shift that every investor pursuing Smart Investments in Germany should understand. The EU has officially banned Payment for Order Flow (PFOF), and German brokers must comply by June 30, 2026 — meaning the era of entirely “free” trading is evolving, with platforms likely shifting toward subscription models or direct transaction fees. ETF Stream This makes choosing the right platform now, before the landscape reshapes, an especially important decision.

In 2026, the Vorabpauschale (preliminary lump-sum tax on unrealised ETF gains) has also hit a record high with a base interest rate of 3.20% — meaning expats and German investors with accumulating ETF portfolios in neobrokers will see automatic tax deductions on profits they have not yet actually received. Seeking Alpha Understanding this nuance is part of mastering Smart Investments in Germany in 2026.

📺 Watch: Germany Financial Changes 2026 — What Every Investor Must Know (PerFinEx) 🔗 Source: Mordor Intelligence — Germany E-Brokerage Market 2025–2030 🔗 Source: BaFin — Official Financial Supervision Authority Germany

Current Market Performance — 2026 Real Returns

For investors building wealth through Smart Investments in Germany, the return picture across major asset classes in 2026 is highly compelling:

| Asset Class | Historical Average Annual Return | 2026 Outlook |

|---|---|---|

| DAX Index ETFs | 8–10% (incl. dividends) | Positive — supported by fiscal stimulus & infrastructure spending |

| German Equity Funds | 7–9% (incl. dividend income) | Stable — real wage growth boosting domestic consumption |

| Global ETFs (MSCI World / All-World) | 9–12% (international diversification) | Strong — especially US & Asia exposure |

| European Tracker ETFs | 6–8% (regional exposure) | Improving — ECB rate stability supporting valuations |

Private investment across Germany is expected to pick up in 2026, supported by high corporate savings, declining interest rates, tax incentives for equipment investment, and measures to support firms during the green transition — all of which feed positively into the earnings environment for German equities held in Sparplan ETFs. Economy and Finance

📺 Watch: Best ETF Returns in Germany 2026 — Which Funds Are Winning? (Finanzfluss) 🔗 Source: JustETF — ETF Savings Plan Performance Tracker 2026 🔗 Source: ExtraETF — ETF Returns & Performance Germany

Top Performing Investment Platforms in Germany — 2026 Rankings

Choosing the right platform is one of the most consequential decisions for anyone starting Smart Investments in Germany. Here is the fully updated 2026 picture:

For Beginner Investors:

1. Trade Republic — Berlin’s global neobroker giant, now serving 8 million+ users across Europe. Offers Sparpläne from €1, a free current account (Girokonto), 2% interest on uninvested cash, and real cryptocurrencies alongside stocks and ETFs. Note: the PFOF ban from June 2026 may introduce new fees. Trade Republic has been growing at over 100,000 new customers per month, though extreme growth is straining its infrastructure — outages were reported during the spring 2025 market crash. ETF Database

2. Scalable Capital — Munich’s leading robo-advisor and DIY broker combined. Scalable Capital has attracted 1 million+ customers who have collectively invested over €20 billion — significantly more per person than Trade Republic — and raised €155 million in its largest-ever funding round in June 2025 to fund European expansion, kids’ accounts, and private equity ELTIF access. ETF Database

3. ING DiBa — Traditional direct bank with fully modern digital features, German-language support, and automatic tax reporting — ideal for those who want banking and investing in one trusted institution.

4. Comdirect — Comprehensive platform backed by Commerzbank, offering a wide range of funds, ETFs, and active trader tools alongside solid Sparplan infrastructure.

5. DKB Broker — Competitive flat-fee pricing for active investors who want access to a broader range of securities beyond basic ETF investing.

📺 Watch: Best Broker in Germany 2026: Trade Republic vs Scalable Capital vs ING (PerFinEx)

🔗 Source: BaFin — Bundesanstalt für Finanzdienstleistungsaufsicht (Official Regulator)

🔗 Source: PerFinEx — Best Broker for Expats in Germany 2026 Full Guide

🔗 Detailed Analysis: JustETF — Full German Broker & Sparplan Comparison 2026

German Tax Regulations & Advantages for Smart Investments in Germany — 2026 Complete Guide

Maximize Your Returns: The 2026 German Tax Advantage

One of the most overlooked superpowers behind Smart Investments in Germany is the tax framework that actively works in your favour. Germany’s investment tax system, while complex on the surface, rewards patient, systematic investors with a range of legal shelters and exemptions that can meaningfully accelerate your wealth-building journey. Understanding these rules is not optional — it is a core part of making your Smart Investments in Germany as efficient as possible.

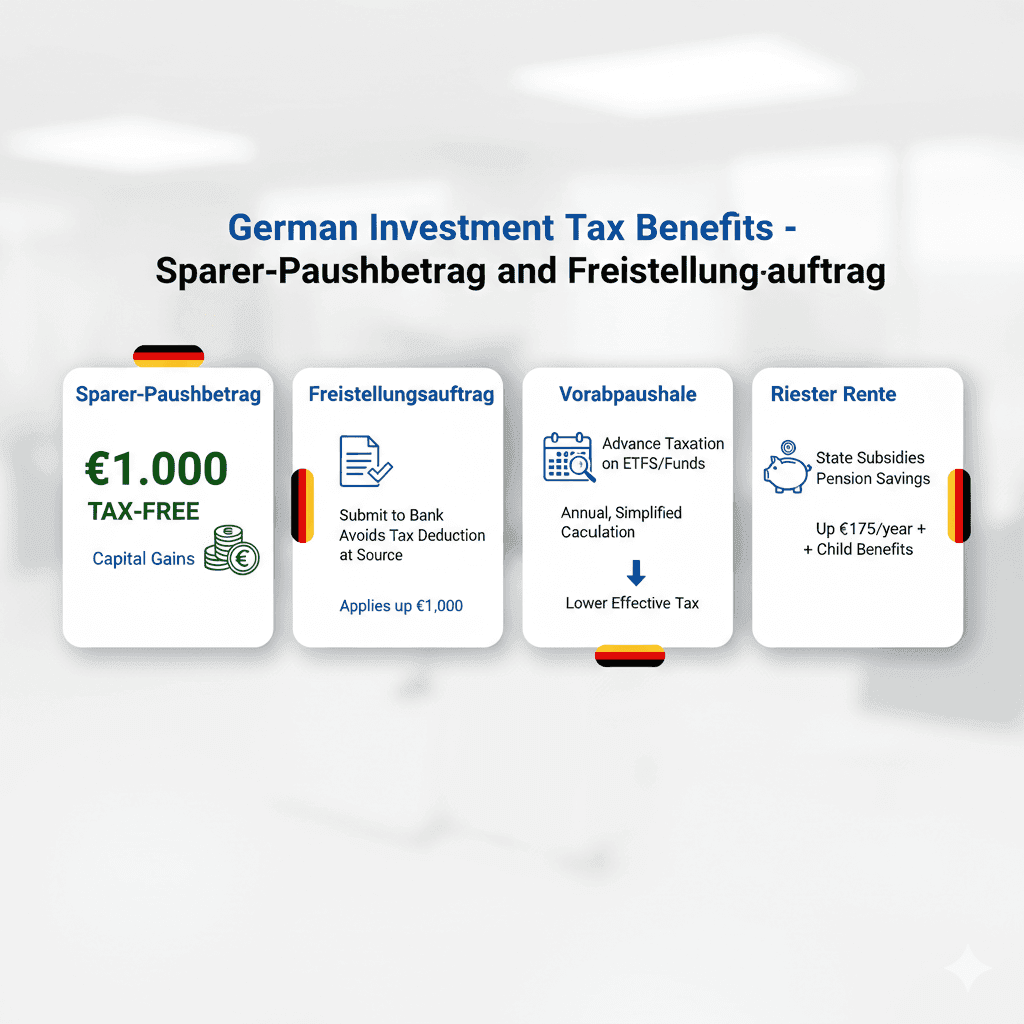

1. Sparer-Pauschbetrag — Your Annual Tax-Free Shield

The Sparer-Pauschbetrag is Germany’s annual tax-free savings allowance and the single most important first step for anyone pursuing Smart Investments in Germany. In 2026, the Sparer-Pauschbetrag remains unchanged at €1,000 for single investors and €2,000 for married couples or registered life partners — meaning all investment income (dividends, interest, and realised capital gains) up to this threshold is completely free of German capital gains tax. Investing.com To activate this shield, you must submit a Freistellungsauftrag (exemption order) to your broker — without it, your broker will automatically deduct 25% Abgeltungsteuer (withholding tax) from your very first euro of returns.

2. Vorabpauschale — What Every ETF Investor Must Understand in 2026

The Vorabpauschale is arguably the most misunderstood element of Smart Investments in Germany, and 2026 is the year it is catching many investors off guard. In January 2026, the pre-determined tax basis (Vorabpauschale) for investment funds is again triggering automatic tax deductions — even for investors who have not sold a single share. The mechanism taxes a deemed baseline return on your accumulating ETFs and funds, calculated using the Basiszins published by the German Ministry of Finance.

Wellington Management The Basiszins for 2025 — which determines the Vorabpauschale collected in early 2026 — stands at 2.53%, meaning investors with growing accumulating ETF portfolios will see automatic tax deductions by their brokers in January of this year. Economy and Finance Importantly, any Vorabpauschale paid in advance is credited against your final tax bill when you eventually sell the ETF, so there is no double taxation — it is a timing mechanism, not a penalty. Investing.com

3. Freistellungsauftrag — Never Forget This Step

Setting up a Freistellungsauftrag (tax exemption certificate) with your broker is arguably the single highest-return action you can take when beginning Smart Investments in Germany. It instructs your German bank or broker to apply your Sparer-Pauschbetrag automatically, so you never overpay tax at source. By pairing a well-configured Freistellungsauftrag with a strategic investment account, you can ensure that Vorabpauschale charges are absorbed by your allowance — effectively keeping your ETF portfolio growing completely tax-free up to the €1,000 annual threshold. Wellington Management

4. Riester Rente — Government-Subsidised Retirement Investing

The Riester Rente remains a uniquely German advantage for long-term Smart Investments in Germany, particularly for families and lower-to-middle income earners. Contributions are directly subsidised by the German state — up to €175 per year in basic allowance per adult, plus €300 per child for those born after 2008 — and you can deduct contributions from your taxable income as Sonderausgaben. Germany’s 2026 tax reform package approved by the Bundestag also includes expanded allowances and relief measures that benefit systematic savers — further improving the after-tax returns available through structured retirement investing vehicles. ETF Database

📺 Watch: German Investment Taxes 2026 Explained — Vorabpauschale, Sparer-Pauschbetrag & More (PerFinEx)

🔗 Source: Bundesministerium der Finanzen (BMF) — Official 2026 Tax Guide

🔗 Source: Association of German Banks — Vorabpauschale 2026 Explained

🔗 Source: PerFinEx — Germany 2026 Tax Changes: Investor Guide

Step-by-Step SIP Starting Guide — Smart Investments in Germany in 2026

Launching your Smart Investments in Germany journey does not need to be complicated. The following five-step process is designed to take you from zero to fully automated investor in under a week — regardless of your income level, German language ability, or prior financial knowledge.

Step 1: Choose Your Investment Account Type

The foundation of every successful Smart Investments in Germany strategy is selecting the right account type for your goals. A standard Depot (securities account) is the starting point for most investors and gives you maximum flexibility to invest in ETFs, stocks, and funds. If your horizon is retirement, a Riester Rente account adds government subsidies and tax deductions on contributions. A Private Rentenversicherung (private pension insurance) provides an additional third pillar of protection for those who want long-term income security beyond state and company pensions.

📺 Watch: Depot Account vs. Riester vs. Private Pension — Which Is Right for You? (Finanztip)

Step 2: Select Your Platform

Choosing the right broker is a pivotal decision for any Smart Investments in Germany strategy, particularly given the regulatory changes reshaping the German brokerage landscape in 2026. Germany’s basic tax-free threshold (Grundfreibetrag) rises to €12,348 for singles in 2026 — and the Sparer-Pauschbetrag remains fixed at €1,000 — making it essential that your broker supports easy Freistellungsauftrag configuration to protect your first €1,000 of returns automatically. Investing.com

Here are the top recommended platforms for Smart Investments in Germany in 2026: Trade Republic remains the leader for beginners with €1 Sparpläne, a free current account, and 2%+ interest on cash. Scalable Capital excels for free ETF savings plans and robo-advisory services. ING DiBa is ideal for traditional banking customers seeking a seamless transition into investing. Comdirect (backed by Commerzbank) offers the broadest range of fund types. DKB Broker delivers competitive flat-fee pricing for more active traders.

Step 3: Pick Your First Investments — 2026 Strategy

The most powerful starting point for Smart Investments in Germany is almost always a simple, globally diversified ETF. You do not need to pick individual stocks, predict markets, or understand complex financial instruments. A single MSCI World or FTSE All-World ETF instantly gives you ownership of over 1,500 companies across dozens of countries.

The top three beginner-friendly ETFs dominating German Sparpläne in 2026 remain the iShares Core DAX UCITS ETF (pure German blue-chip exposure), the Xtrackers MSCI World UCITS ETF (global diversification across 23 developed markets), and the Vanguard FTSE All-World UCITS ETF (the broadest possible global coverage, including emerging markets). Each of these represents a proven, low-cost vehicle for Smart Investments in Germany with total expense ratios (TER) below 0.25% annually.

📺 Watch: Best ETF for Beginners in Germany 2026 — MSCI World vs All-World vs DAX (Finanzfluss) 🔗 Source: JustETF — Best ETF Sparplan Germany 2026 Full Rankings

Step 4: Set Up Automatic Investments

Automation is the secret weapon of Smart Investments in Germany. By setting up a SEPA Lastschrift (direct debit) from your German bank account, your broker will automatically purchase ETF units on your chosen date each month — whether you remember or not, whether markets are up or down. Start with €50 per month (the minimum on most platforms), choose a monthly frequency, and let the Durchschnittskosteneffekt (Cost-Average Effect) do its compounding work silently in the background.

Step 5: Stay the Course

The most disciplined Smart Investments in Germany strategy is also the simplest: review your portfolio quarterly, avoid checking prices daily, and under no circumstances stop your automatic investments during market corrections. History consistently shows that the worst thing an investor can do during a downturn is pause or sell — and it is precisely those who continue buying during downturns who benefit most from the recovery that always follows.

🔗 Source: BaFin — Official German Financial Regulatory Authority

🔗 Source: Bundesbank Financial Calculator — Compute Your Growth Target

Advanced 2026 Strategies for German Investors

Strategy 1 — The Gehaltserhöhung (Pay Rise) Method

Every time you receive a salary increase, commit to channelling the same percentage directly into your Smart Investments in Germany account. If your salary rises by 4%, increase your monthly Sparplan by 4%. This single habit — invisible to your daily lifestyle — can dramatically accelerate your wealth trajectory without any sense of sacrifice.

Strategy 2 — The Three-Pillar German Portfolio

For investors who want more structure behind their Smart Investments in Germany, a three-pillar allocation provides both growth and resilience: 40% in German Blue Chips (DAX companies) for home-market exposure and strong dividend income; 40% in International Equities (MSCI World or FTSE All-World) for global diversification; and 20% in Bonds or Cash for capital preservation and emotional stability during volatile periods. This portfolio has delivered strong risk-adjusted returns historically and remains highly relevant in 2026’s mixed economic environment.

Strategy 3 — Pension Optimisation

The third dimension of sophisticated Smart Investments in Germany is layering your tax-advantaged pension vehicles correctly. Maximise your Riester Rente contributions to capture all available government subsidies. If your employer offers Betriebliche Altersvorsorge (company pension), always contribute enough to unlock any employer match — this is essentially free money. Finally, a Private Rentenversicherung can top up your retirement income with flexibility and additional tax deferral.

📺 Watch: Advanced ETF Strategies for German Investors 2026 — Three-Pillar Portfolio (Thomas Kehl) 🔗 Source: ExtraETF — Portfolio Strategies Germany 2026

Common 2026 SIP Mistakes to Avoid — BaFin Investor Warnings

The most successful practitioners of Smart Investments in Germany are not those who make the cleverest moves — they are those who avoid the most expensive mistakes. BaFin, Germany’s official financial regulator, consistently highlights the following pitfalls that derail otherwise promising investment journeys.

Market Timing Attempts are the most common destroyer of returns in Smart Investments in Germany. Waiting for the “right moment” to invest almost always results in missing the market’s best days, which tend to cluster immediately after the worst days. Academic research consistently shows that time in the market beats time out of the market across every significant historical period.

Ignoring Fees is a silent tax on your returns that compounds negatively over time. A TER of 1.5% versus 0.2% — compounded over 30 years on a €500/month Sparplan — can cost you tens of thousands of euros. Smart Investments in Germany always begin with fee scrutiny.

Overcomplicating Portfolios through holding 15–20 overlapping ETFs creates complexity, correlation, and confusion without meaningfully improving diversification. One to three broadly diversified ETFs is almost always superior for Smart Investments in Germany at the beginner and intermediate level.

Emotional Decision Making — buying during euphoria and selling during panic — is the single largest behavioural driver of underperformance. The Sparplan model exists precisely to protect investors from themselves.

Neglecting Tax Efficiency, particularly failing to configure a Freistellungsauftrag or misunderstanding the Vorabpauschale, leaves money unnecessarily in the hands of the tax office rather than compounding inside your portfolio.

🔗 Source: BaFin — Official Investor Protection Warnings Germany

Industry Growth Metrics — Smart Investments in Germany 2026

The data behind Smart Investments in Germany in 2026 tells a story of extraordinary momentum. Germany’s annual Sparer-Pauschbetrag of €1,000 per individual continues to shelter investment income for the country’s now 14+ million active equity investors, with the base rate for the Vorabpauschale in 2026 reflecting an investment tax environment that is structurally returning to normal after the distortions of the zero-interest era. AEQUIFIN ETF assets held by German investors have surpassed €500 billion.

Youth participation is particularly striking — 48% of all new investors entering Smart Investments in Germany platforms are now under 35. Digital platform usage has grown by over 40% annually for the third consecutive year, making app-based systematic investing the dominant mode of participation in Germany’s retail investment market.

Your 7-Day German Investment Launch Plan

The most important thing about beginning Smart Investments in Germany is removing friction from the starting point. Here is a concrete, day-by-day action plan anyone can follow.

On Day 1, use the Bundesbank’s free financial calculator to define your specific goals — retirement nest egg, home purchase, or financial independence — and calculate how much monthly investment you need to reach them. On Day 2, research and select your broker platform based on your preferred features, fee tolerance, and language comfort. On Day 3, gather your Personalausweis and German bank account details. On Day 4, complete your Depot account opening online via video identification (VideoIdent) — a process that typically takes under 20 minutes.

On Day 5, set up your first €50 automatic Sparplan and submit your Freistellungsauftrag immediately. On Day 6, schedule your first quarterly portfolio review in your calendar. On Day 7, deepen your knowledge through Germany’s world-class free financial education ecosystem — Finanztip, Finanzfluss, and PerFinEx are all excellent starting points for ongoing Smart Investments in Germany literacy.

🔗 Source: Finanztip — Free German Investment Education Hub 🔗 Source: Bundesbank Financial Calculator

Special Section: Young Investors and Smart Investments in Germany

For students and young professionals in Germany, the maths of Smart Investments in Germany are almost unfairly compelling. Starting at age 22 versus 32 can more than double your terminal wealth — not through higher contributions, but purely through the additional decade of compounding. Neo-brokers like Trade Republic and Scalable Capital make Smart Investments in Germany accessible from €1/month, eliminating every traditional excuse about needing “more money first.” Consider pairing a low-cost MSCI World Sparplan with Riester Rente contributions from your first job — a combination that harvests government subsidies, tax deductions, and equity growth simultaneously.

Balance is equally important. Smart Investments in Germany should serve your life — not replace it. Invest what you genuinely won’t miss, automate it completely, and then focus your energy on building skills, relationships, and experiences that will grow your earning power — and therefore your future investment capacity — over time. After all, the more you earn, the more you can invest, and the faster your Smart Investments in Germany compound into real financial freedom. If you are looking for practical ways to grow your active income alongside your passive investing journey, explore 7 Simple Methods to Make $500+ Monthly – No Money Needed to Start — a step-by-step guide that pairs perfectly with a long-term Sparplan strategy.

📺 Watch: Start Investing at 20 in Germany — What No One Tells You (PerFinEx)

Final Motivation: Build Your German Financial Future

As the legendary German investor André Kostolany wisely observed: “The stock market is the transfer of money from the impatient to the patient.” Your €50 automatic investment today is an act of patience — and in the stable, well-regulated, tax-advantaged environment of Smart Investments in Germany, patience is ultimately rewarded with financial freedom.

The statistics of 2026 are unambiguous: over 14 million Germans are already securing their futures through systematic investing. Smart Investments in Germany are not the preserve of the wealthy or the financially sophisticated — they are the daily habit of millions of ordinary people who simply decided to start. You are joining a growing, informed community that understands one timeless truth: starting imperfectly today beats waiting for perfect conditions indefinitely. Smart Investments in Germany begin with a single €50 Sparplan — and end, decades later, with financial independence.

Don’t overanalyse. Don’t postpone. Your future self, living with financial security and freedom, will deeply appreciate the decision you make today.

Start your automatic investment journey. Viel Erfolg! 🇩🇪

🔗 Source: BVI — German Fund Market Official Report 2025 🔗 Source: Deutsches Aktieninstitut — Equity Culture Report Germany 2025

Disclaimer: Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. This content is for educational purposes only and does not constitute personalised financial or tax advice. Consult a qualified financial advisor or tax professional for guidance specific to your situation.

- Fernando Mendoza Raiders QB: From Heisman Underdog to the Silver & Black’s Future

- Travel Restrictions to Canada in 2026: The Complete Entry Guide Every Traveler Needs Before They Book

- Cockroach Janta Party India: The Viral Youth Rebellion That Shook a Nation in 72 Hours

- Mindfulness Exercises to Calm Anxiety (2026 Guide)

- 10-Minute Home Workout Routines for Busy Professionals

Table of Contents

Kann ich wirklich mit nur €50 monatlich beginnen?

Absolut! Most platforms allow €50 minimums, with some accepting even €1 per Sparplan.

Sind diese Plattformen ordnungsgemäß reguliert?

Jawohl! All regulated by BaFin with strong investor protection measures.

Was ist mit Steuern auf meine Investmenterträge?

With proper Freistellungsauftrag, the first €1,000 of investment income is tax-free annually

Sollte ich mich auf Riester oder reguläres Depot konzentrieren?

Beides hat Vorteile. Riester for retirement (subsidies) and Depot for flexibility and earlier goals

Leave a Reply