Introduction: SIP Investing in Canada 2026

Hey There, Future Millionaires!

Living in Canada gives you access to some of the world’s best investment opportunities, eh? But if your money is sitting in a savings account earning next to nothing, you are missing out on serious growth potential. With over 7 million Canadians now investing regularly through digital platforms — and Wealthsimple alone crossing $100 billion in assets under administration by early 2026 — there has never been a better time to grow your wealth systematically. (Source: Wealthsimple 2025 Annual Update)

Welcome to SIP Investing in Canada — the smart, automated way to build your financial future without needing to be a Bay Street expert. Whether you are a teacher in Ontario, an oil worker in Alberta, a tech professional in BC, or a retiree in Quebec, SIP Investing in Canada is your proven pathway to long-term financial security. The strategy works beautifully inside registered accounts like your TFSA, RRSP, and the newer First Home Savings Account (FHSA) — all of which carry fresh 2026 contribution limits you should know about.

The best part? You can start with just $100 per month. Let’s get started, right?

📺 Watch this first: How to Start Investing in Canada for Beginners (2026) – YouTube

For our international readers, check out our global investment guides.

What is SIP Investing in Canada? The Canadian Way

SIP (Systematic Investment Plan) — or what we officially call “Pre-Authorized Contributions (PACs)” or “Automatic Investment Plans” in Canada — is your set-it-and-forget-it strategy to build wealth consistently. It is not a specific product, but rather a disciplined approach of investing fixed amounts at regular intervals (weekly, monthly, or quarterly), regardless of whether markets are up or down. SIP Investing in Canada works the same way the rest of the world uses the term, just with a Canadian twist in terminology.

Classic Canadian Example: Think of buying maple syrup. When it is on sale, you stock up. When prices are at regular levels, you buy exactly what you need. Over time, your average cost balances out beautifully. That is Dollar Cost Averaging (DCA) — the cornerstone principle that makes SIP Investing in Canada so powerful and psychologically stress-free for everyday investors.

As of March 2026, here is what makes the SIP approach especially powerful in Canada’s current environment:

The CRA has confirmed the TFSA contribution limit for 2026 at $7,000, and if you have been eligible since the TFSA launched in 2009 and have never contributed, your cumulative room has now reached an incredible $109,000 in tax-free space. (Source: Canada.ca — Calculate Your TFSA Contribution Room) Automating your SIP Investing in Canada strategy to hit that $7,000 ceiling is as simple as setting aside $583.33 per month — a perfect auto-contribution amount.

On the RRSP side, the 2026 contribution limit has risen to $33,810 (up from $32,490 in 2025), giving higher-income earners even more room to reduce taxable income while building retirement wealth through systematic contributions. (Source: The Globe and Mail — New Canadian Laws and Rules in 2026)

Additionally, the Carney government’s new federal income tax rate of 14% (reduced from 15%) on the lowest bracket, effective for the full year in 2026, means Canadians are keeping slightly more of their hard-earned money — making it even easier to fund a monthly SIP contribution without feeling the pinch.

📺 Watch: Dollar Cost Averaging Explained Simply – Canada (YouTube)

SIP Investing in Canada is not just about picking a stock or a fund — it is about building the habit of investing. Platforms like Wealthsimple, Questrade, and CIBC Investor’s Edge all offer automated recurring investment features that make setting up your SIP plan a 5-minute process. (Source: CIBC Investor’s Edge — Regular Investment Plans) Wealthsimple, Canada’s leading commission-free platform, even offers Recurring Buys on eligible ETFs and stocks — making it the go-to platform for first-time SIP investors in 2026.

📺 Watch: Wealthsimple Auto-Invest Tutorial for Canadians – YouTube

The bottom line is this: whether you are brand new to the markets or a seasoned saver looking to automate your strategy, SIP Investing in Canada remains the single most accessible, low-stress, and statistically reliable method to grow long-term wealth in the current 2026 economic environment. Start small, stay consistent, and let compounding do the heavy lifting.

💡 Calculate Your Potential

Use the Government of Canada Compound Interest Calculator to see how just $200/month can grow into over $1 million in 40 years — that is the power of time and consistency working together. SIP Investing in Canada turns this mathematical magic into an everyday reality.

📺 Watch this: How Compound Interest Actually Works in Canada — YouTube

Why 2026 is the Smart Time for SIP Investing in Canada

The Canadian Economic Landscape — March 2026 Reality Check

Before you invest a single dollar, you need to understand the environment you are investing into. The good news is that, despite some real headwinds, the overall picture for systematic investors is encouraging — and here is why.

GDP Growth is forecast at approximately 1.4–1.8% for 2026, according to both Vanguard Canada and the Bank of Canada’s latest Monetary Policy Report. Core inflation eased through late 2025, giving the Bank of Canada room to cut rates by a cumulative 100 basis points, and the BoC held its policy rate at 2.25% in January 2026 as it weighs softer hiring against gradually improving macro conditions. MoneySense (Source: Vanguard Canada Economic Outlook 2026)

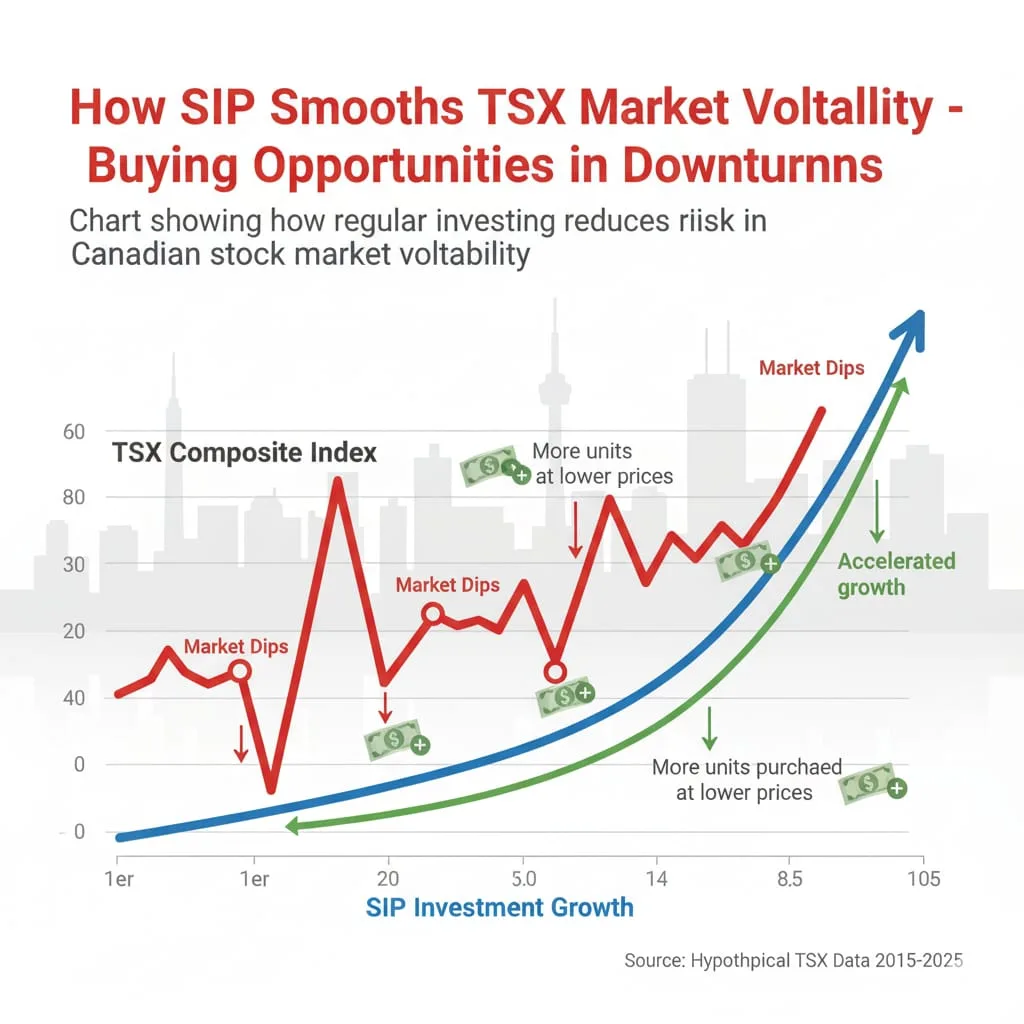

Yes, growth is modest — and that is actually good news for SIP Investing in Canada. Slower, more cautious markets mean you get to buy more units of your chosen ETFs or funds at lower prices during your early contribution years. That is dollar cost averaging doing exactly what it should.

Inflation is projected to remain close to the Bank of Canada’s 2% target through 2026. The effects of weaker demand on the economy are anticipated to mostly offset the inflationary pressures caused by tariffs, keeping inflation projected to remain close to 2%. Yahoo! (Source: Bank of Canada — Canadian Outlook, MPR 2025) Stable inflation preserves the real purchasing power of your invested dollars — a core reason to stay consistent with your monthly SIP contributions.

Market Strength is perhaps the most exciting data point of all. The S&P/TSX Composite Index closed 2025 with a remarkable 28.3% price return for the full year StockBrokers, and as of late February 2026, the TSX capped a volatile week with a 1.5% gain and a monthly advance of 7.6%, even while retreating slightly from a record high. Google Play (Source: Trading Economics — TSX Live Data) For anyone who stayed invested through 2025 via automated SIP Investing in Canada contributions, the results speak for themselves.

The Bank of Canada’s overnight rate stands at 2.25% as of end-2025, after a cumulative easing of 1.75% — and monetary policy easing and fiscal stimulus are seen as important drivers that could boost growth in 2026 beyond current estimates. Yahoo! (Source: RBC Global Asset Management — Canada 2026 Outlook) Lower rates mean borrowing costs are falling, consumer spending is picking up, and equities remain attractive relative to cash savings. This environment rewards investors who automate their contributions rather than waiting on the sidelines.

📺 Watch: Bank of Canada Rate Cuts — What It Means for Canadian Investors — YouTube

The Digital Investment Boom — Canada in 2026

The infrastructure for SIP Investing in Canada has never been more accessible or beginner-friendly. Over 7 million Canadians now invest through digital platforms, and auto-investing features are standard on every major Canadian platform. Fractional shares have made blue-chip stocks like Shopify, Royal Bank, and Canadian Natural Resources accessible to anyone starting with as little as $1. (Source: IIAC Digital Investment Report)

Platforms like Wealthsimple, Questrade, and BMO InvestorLine all support Pre-Authorized Contribution plans (PACs) that automate your SIP Investing in Canada strategy completely — you set the amount, set the frequency, and let the market do the rest. Wealthsimple’s Recurring Buys feature, available on ETFs and stocks, remains the most frictionless entry point for new systematic investors in 2026.

📺 Watch: Wealthsimple vs Questrade — Which is Better for Auto-Investing in Canada? — YouTube

Current Market Performance — March 2026 Real Data

Here is an honest, up-to-date picture of what Canadian and international funds are delivering for SIP investors right now:

TSX Composite Index Funds delivered a total return of approximately 28.3% in 2025 (price return), with a long-term historical average of around 9–10% annually including dividends. As a cornerstone of any SIP Investing in Canada strategy, a low-cost TSX index ETF like iShares XIC remains the default starting point for most beginners. (Source: iShares XIC — BlackRock Canada)

Canadian Equity Funds (actively managed, including dividend income) have historically delivered 8–11% annually over 10-year rolling periods, though 2025 was an exceptional year that pushed those averages higher.

Global ETFs tracking the MSCI World or S&P 500 continue to deliver 9–12% historically, and in 2025 the S&P 500 also posted strong gains. Diversifying your SIP Investing in Canada contributions across both domestic TSX funds and global ETFs is the approach endorsed by most Canadian certified financial planners.

Dividend Growth Funds typically return 5–7% annually but offer the psychological comfort of regular income — making them especially popular for SIP investors within TFSAs and RRSPs who reinvest those dividends automatically. (Source: MoneySense — Best Canadian ETFs 2026)

📺 Watch: Best ETFs for Canadians in 2026 — Complete Beginner Guide — YouTube

Top Performing Investment Platforms for SIP Investing in Canada (March 2026)

The right platform is the engine of your entire SIP Investing in Canada system. Here are the trusted options ranked by accessibility and features in 2026:

Wealthsimple remains Canada’s most popular commission-free platform for automated investing, with Recurring Buys on ETFs and a seamlessly integrated TFSA/RRSP/FHSA setup. (Source: Wealthsimple.com)

Questrade offers the most flexibility for self-directed investors, with ETF purchases at zero commission and powerful pre-authorized contribution tools. (Source: Questrade.com)

Justwealth is the top-rated robo-advisor for RESP accounts specifically, using target-date funds that automatically de-risk as your child approaches post-secondary age — a smart addition to any family’s SIP strategy. (Source: Cut The Crap Investing — Justwealth Review)

BMO InvestorLine / CIBC Investor’s Edge are strong choices for investors who prefer banking within a Big Six institution while still accessing automated contribution plans. (Source: CIBC Investor’s Edge — Regular Investment Plans)

📚 Trusted Sources & Further Reading

Here is a curated reference list to bookmark as you build your SIP Investing in Canada knowledge base:

Bank of Canada — Monetary Policy Report, January 2026 | RBC Wealth Management — Canada 2026 Economic Outlook | Vanguard Canada — 2026 Economic Forecast | MoneySense — Best ETFs Canada 2026 | BDC — Canada Economic Outlook 2026 | The Globe and Mail — TSX Composite Live Data | iShares XIC ETF — BlackRock Canada

For Beginner Investors:

- Wealthsimple: Canada’s leading robo-advisor and trading platform

- Questrade: Popular for low-cost ETF investing

- RBC Direct Investing: Full-service banking integration

- TD EasyTrade: Commission-free trading for beginners

- BMO InvestorLine: Comprehensive investment platform

Official Source: Canadian Securities Administrators (CSA)

CRA Regulations and Tax Advantages for 2025

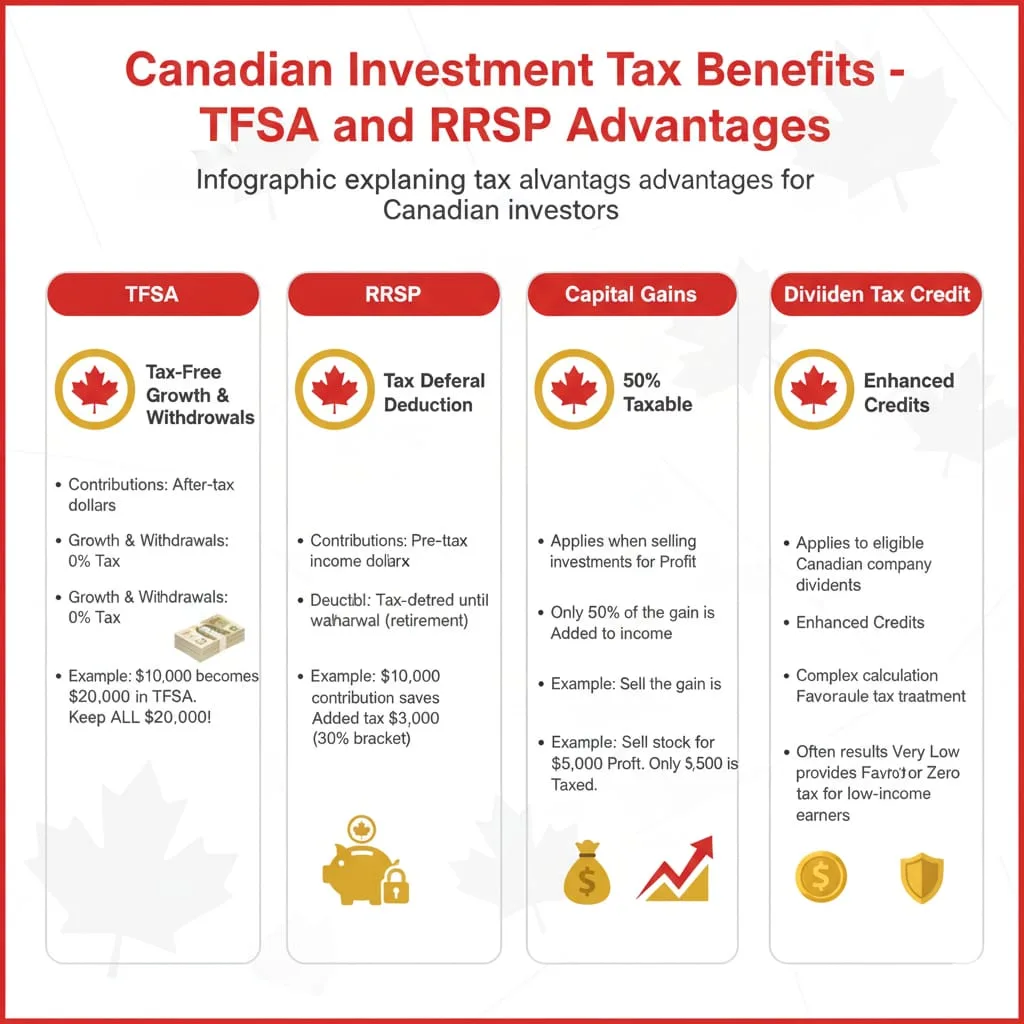

Maximize your returns with these Canadian tax benefits:

- TFSA Limit: $7,000 annual tax-free investing for 2025

- RRSP Deductions: Tax-deferred growth and contribution deductions

- Capital Gains Inclusion: 50% of gains tax-free

- Dividend Tax Credit: Enhanced credits for Canadian dividends

Official Source: Canada Revenue Agency (CRA) Investment Guide

Step-by-Step SIP Starting Guide 2025

Step 1: Choose Your Investment Account Type

- TFSA: Tax-free growth for all investments

- RRSP: Tax-deferred retirement savings

- Non-Registered Account: For investments beyond registered limits

💡 Calculate Your Potential

Use the Government of Canada Compound Interest Calculator to see how just $200/month can grow into over $1 million in 40 years at a 9% average annual return. That is the mathematical engine behind SIP Investing in Canada — patience, consistency, and compounding doing the work so you do not have to.

📺 Watch: How Compound Interest Works in Canada — Beginner Example (YouTube)

Step 2: Select Your Platform — March 2026 Updated Guide

The platform landscape in Canada has changed dramatically by early 2026, and picking the right one is one of the most important decisions in your SIP Investing in Canada journey. The great news is that the race to zero-commission trading is now complete — both Wealthsimple and Questrade now offer commission-free trades on Canadian and US-listed stocks and ETFs, a massive shift that levelled the playing field. T Futu Newshat means your choice is no longer about who is cheapest but about which experience fits how you invest.

Here is a clear breakdown of the top platforms as of March 2026:

1. Wealthsimple — Best for Beginners and Automated SIP Investing is the go-to choice for most first-time systematic investors in Canada. Its automatic weekly or monthly deposit feature combined with fractional shares and zero commissions makes it ideal for passive, buy-and-hold investors who want to set a recurring contribution and never think about it again. T Scrivenshe mobile app is considered the cleanest and most intuitive in Canada, making it especially powerful for anyone managing their investments from their phone. All major registered accounts — TFSA, RRSP, FHSA, and RESP — are fully supported. (Source: Wealthsimple.com)

2. Questrade — Best for Self-Directed and US-Heavy Investors is the stronger option if you plan to hold US-listed stocks or ETFs regularly. Questrade wins for USD trading through Norbert’s Gambit, which allows savvy investors to convert CAD to USD at roughly 0.2% — far cheaper than Wealthsimple’s standard 1.5% FX fee. Q IG Wealth Managementuestrade also offers real-time market data, options trading, and advanced charting tools that more experienced investors will appreciate. (Source: Questrade.com)

3. Qtrade — Best Overall for Long-Term DIY Investors has emerged as a dark horse worth serious consideration in 2026. Qtrade now also offers completely free trades on stocks and ETFs while being praised for its world-class customer service — a feature that more and more Canadians are prioritizing as they switch away from the big banks. I The Globe and Mailt also supports full Dividend Reinvestment Plans (DRIPs), which Wealthsimple does not, making it a stronger pick for dividend-focused SIP investors. (Source: Million Dollar Journey — Qtrade Review 2026)

4. RBC Direct Investing remains an excellent choice for those who already bank with RBC and want the simplicity of having their chequing, savings, TFSA, and RRSP all under one roof. The integration makes setting up Pre-Authorized Contributions (PACs) seamless. The trade-off is higher fees relative to Wealthsimple and Questrade, which matters more as your portfolio grows. (Source: RBC Direct Investing)

5. BMO InvestorLine rounds out the Big Bank options with one of the most comprehensive research libraries of any Canadian platform, including access to analyst reports and portfolio planning tools. For investors who want institutional-quality data to support their SIP Investing in Canada strategy, BMO InvestorLine delivers. (Source: BMO InvestorLine)

📺 Watch: Best Investment Platforms in Canada 2026 — Wealthsimple vs Questrade vs Qtrade (YouTube)

Security note for all platforms: Both Wealthsimple and Questrade are regulated in Canada, and your funds are protected by the Canadian Investor Protection Fund (CIPF) up to $1 million per account category in the event your brokerage fails. Yo Yahoo!ur money is safe on any of the platforms listed above.

Step 3: Pick Your First Investments — 2026 Strategy for SIP Investing in Canada

For the vast majority of Canadians beginning their SIP Investing in Canada journey, a low-cost index ETF is the single best starting investment. Here is why: instant diversification across hundreds of companies, professional rebalancing built into the ETF structure, rock-bottom management expense ratios (MERs), and decades of proven long-term returns — all wrapped into one ticker symbol you can buy in 30 seconds.

The three most recommended Canadian starter ETFs in 2026 remain:

Vanguard FTSE Canada All Cap Index ETF (VCN) gives you broad exposure to Canadian large, mid, and small-cap stocks in a single fund with an ultra-low MER of just 0.05%. It is the purest expression of the Canadian equity market and a cornerstone of any domestic-focused SIP portfolio. (Source: Vanguard Canada — VCN)

iShares Core S&P/TSX Capped Composite Index ETF (XIC) is BlackRock’s flagship Canadian equity ETF and one of the most widely held index funds in the country, with a similar 0.06% MER. It tracks the S&P/TSX Capped Composite Index and has delivered a long-term historical average annual return of approximately 9–10% including dividends. (Source: iShares XIC — BlackRock Canada)

BMO S&P/TSX Capped Composite Index ETF (ZCN) is BMO’s equivalent offering, priced comparably and equally valid for a beginner systematic investor. If you already bank with BMO, ZCN is the natural starting point.

For investors who want one ETF to rule them all — including both Canadian and global exposure — the Vanguard All-Equity ETF Portfolio (VEQT) and iShares Core Equity ETF Portfolio (XEQT) are the gold standard in 2026. Both hold thousands of global stocks in a single fund, automatically rebalance, and cost less than 0.25% per year to own. They are the simplest, most diversified options available for SIP Investing in Canada and are enthusiastically recommended by the Canadian financial planning community. (Source: MoneySense — Best ETFs Canada 2026)

📺 Watch: XEQT vs VEQT — Which ETF Should You Buy in Canada? (YouTube)

Step 4: Set Up Your Automatic Investments — The Heart of SIP Investing in Canada

This is the step that separates people who talk about investing from people who actually build wealth. Setting up your automatic contributions takes about 5 minutes, and once it is running, it requires no willpower, no timing the market, and no monthly decision-making.

Start with $100–$200 per month — most platforms including Wealthsimple and Questrade have no minimum deposit requirement whatsoever. Choose a monthly contribution frequency to align with your paycheque schedule. Enable a Pre-Authorized Contribution (PAC) directly from your Canadian chequing account, which pulls the funds automatically on the date you choose. Then direct those contributions into your chosen ETF (VCN, XIC, XEQT, or VEQT) and let compounding begin.

On Wealthsimple specifically, the Recurring Buys feature allows you to set a specific dollar amount to automatically purchase your chosen ETF on a set schedule — no manual order placement required, ever. This is the most frictionless implementation of SIP Investing in Canada available today.

📺 Watch: How to Set Up Auto-Invest on Wealthsimple — Step by Step 2026 (YouTube)

Step 5: Stay the Course — The Most Underrated Skill in Investing

Review your portfolio quarterly — not daily. Daily price checking is the enemy of systematic investing because it creates emotional noise around decisions that should be mechanical. Never pause or stop your automatic contributions during market downturns; those are precisely the months when your fixed dollar amount buys more units of your ETF at cheaper prices, which is dollar cost averaging doing exactly what it should. Each time you receive a salary increase, increase your monthly contribution by the same percentage — this maintains your lifestyle while quietly accelerating your wealth accumulation in the background.

Advanced 2026 Strategies for SIP Investing in Canada

Strategy 1 — The Pay Raise Method: Every time your employer gives you a raise, redirect the same percentage increase to your automatic monthly SIP contribution. If you earn a 4% raise, increase your monthly contribution by 4%. You never notice the difference in your take-home pay because the lifestyle upgrade and the investment increase happen simultaneously. This single habit, sustained over a career, is responsible for the majority of the wealth accumulated by middle-income Canadian investors.

Strategy 2 — The Three-Pillar Canadian Portfolio: A more sophisticated approach involves allocating your monthly SIP contributions across three distinct buckets: 40% to Canadian Equities (such as XIC or VCN, which benefit from the Canadian dividend tax credit), 40% to US and International Equities (via XEQT or a separate US index ETF for global diversification), and 20% to Bonds or GICs for capital preservation and to reduce volatility during downturns. This structure is well-suited to investors in their 30s and 40s who want growth with a modest cushion. (Source: Canadian Couch Potato — Model Portfolios 2026)

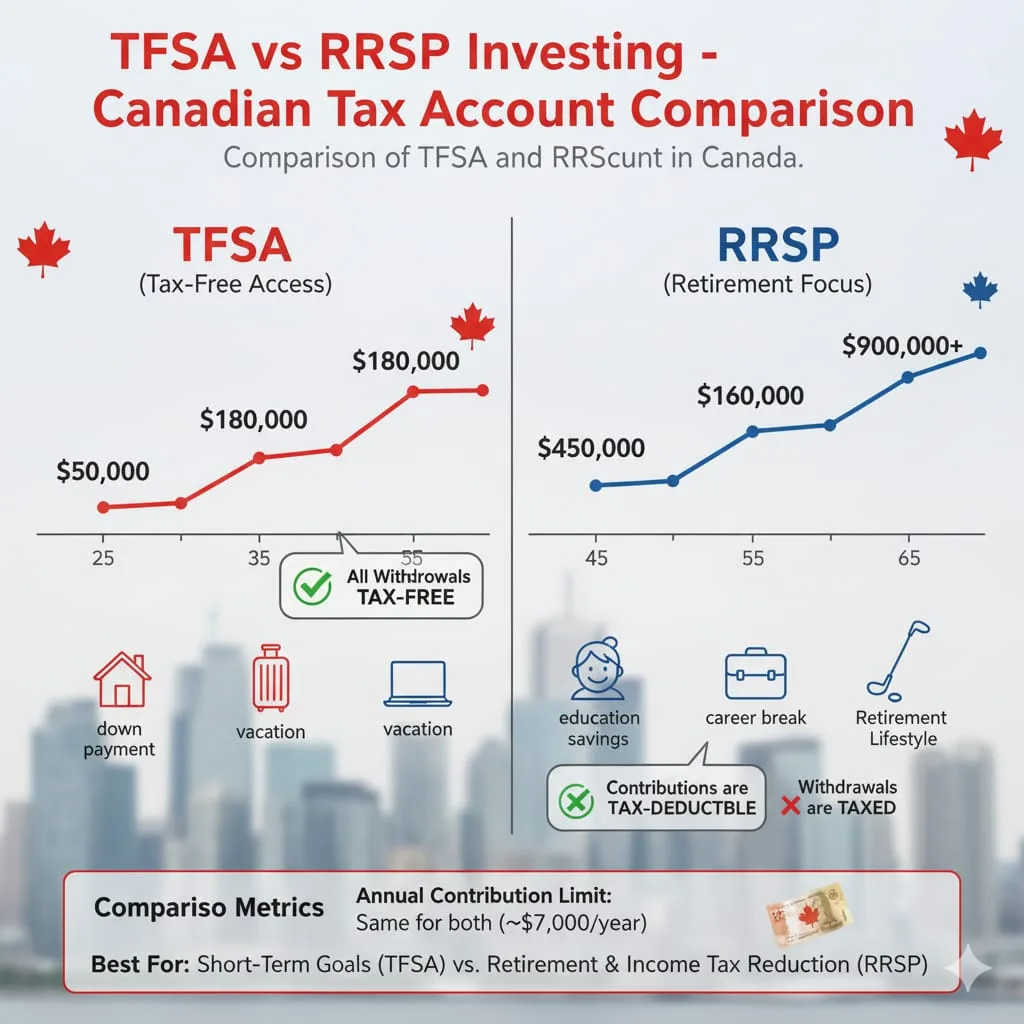

Strategy 3 — Retirement Optimization: A fully optimized SIP Investing in Canada retirement plan in 2026 uses all three registered accounts in combination. Your RRSP (2026 contribution limit: $33,810) provides an immediate income tax deduction and tax-deferred growth — prioritize this if you are in a high tax bracket today. Your TFSA ($7,000 annual limit in 2026, $109,000 cumulative room) grows completely tax-free and provides tax-free income in retirement — prioritize this if you expect to be in a similar or higher tax bracket in the future.

Your FHSA (First Home Savings Account, $8,000 annual limit up to $40,000 lifetime) combines the tax deduction of an RRSP with the tax-free withdrawal of a TFSA — if you are a first-time buyer, maxing this account should be your very first priority before either RRSP or TFSA contributions. And always, always maximize any employer pension matching before directing money anywhere else — that is an immediate 50–100% guaranteed return on every matched dollar. (Source: Canada.ca — TFSA Rules)

📺 Watch: RRSP vs TFSA vs FHSA — Which Should You Prioritize in 2026? (YouTube)

Common 2026 SIP Mistakes to Avoid in Canada (FCAC Investor Guidance)

The Financial Consumer Agency of Canada (FCAC) regularly publishes investor guidance that highlights the most common and costly mistakes that derail otherwise solid systematic investment strategies. Here are the critical ones to avoid as you build your SIP Investing in Canada plan in 2026. (Source: FCAC — Investing Basics)

The biggest mistake is stopping contributions during market corrections. When the TSX dropped sharply in early 2025 due to trade policy uncertainty, investors who paused their PACs locked in losses and missed the subsequent recovery rally that helped push the TSX to its 28.3% full-year return. The entire value of the SIP method comes from buying through those scary months, not around them.

The second most common mistake is holding too much cash in a TFSA savings account rather than investing it. Millions of Canadians have TFSA accounts that hold cash earning 2–3% in a high-interest savings account instead of the 9–10% historical returns available from a simple index ETF. That is a retirement-defining difference over 20–30 years.

The third mistake is ignoring the MER (Management Expense Ratio) of the funds you choose. A 2% MER mutual fund versus a 0.06% ETF seems like a small difference, but on a $500,000 portfolio that gap costs you roughly $9,700 every single year in fees that compound against you. Always check the MER before you buy.

📚 Complete Trusted Source Reference List

Here are all the authoritative Canadian sources to bookmark for your SIP Investing in Canada research:

Government of Canada — Compound Interest Calculator | Canada.ca — TFSA Rules and Contribution Room | FCAC — Savings and Investments Guide | MoneySense — Best ETFs Canada 2026 | Canadian Couch Potato — Model Portfolios | Million Dollar Journey — Platform Reviews 2026 | iShares XIC — BlackRock Canada | Vanguard Canada — VCN ETF | Wealthsimple | Questrade | StockBrokers.com — 2026 Platform Comparison

- Market Timing Attempts: Trying to outsmart markets instead of consistent investing

- Ignoring Fees: Overlooking MERs and trading commissions that erode returns

- Overcomplicating Portfolios: Too many funds creating complexity and overlap

- Emotional Decision Making: Buying during FOMO and selling during panic

- Neglecting Tax Efficiency: Not maximizing TFSA and RRSP advantages

Frequently Asked Questions (2025 Canadian Edition)

Q: Can I really start with just $100 monthly?

A: Absolutely! Most platforms allow $100 minimums, with some accepting even less with micro-investing.

Q: Are these platforms properly regulated?

A: For sure! All regulated by provincial securities commissions with CIPF protection up to $1 million.

Q: What about tax on my investment returns?

A: Within a TFSA, all returns are completely tax-free – no reporting required.

Q: Should I focus on my RRSP or TFSA first?

A: It depends on your income. Generally, RRSP for higher tax brackets and TFSA for lower brackets or flexibility.

Industry Growth Metrics 2026 Canada

- Regular Investors: 6 million+ Canadians investing monthly

- ETF Assets: $400+ billion in Canadian ETFs

- Youth Participation: 45% of new investors under 35

- Digital Platform Growth: 35% annual increase in app-based investing

Your 7-Day Canadian Investment Launch Plan

Day 1: Calculate your goals using FCAC financial tools

Day 2: Research and choose your investment platform

Day 3: Gather your SIN and banking information

Day 4: Open your TFSA or RRSP account

Day 5: Set up first $100 automatic investment

Day 6: Schedule annual portfolio review

Day 7: Continue learning through Canadian financial resources

Special Section: Young Canadian Investors

For Students and Young Professionals:

- Start with micro-investing apps for small regular amounts

- Consider First Home Savings Account (FHSA) for home purchase

- Leverage decades of compounding through early starts

- Balance investing with enjoying your twenties and thirties

Final Motivation: Build Your Canadian Financial Future

As legendary Canadian investor Peter Lynch famously said: “The key to making money in stocks is not to get scared out of them.”

Your $100 automatic investment today embodies that wisdom. In the stable environment of Canada’s financial markets, with strong regulation, global company access, and exceptional tax advantages, your regular investments can grow into a substantial nest egg.

The statistics are clear – over 6 million Canadians are already securing their futures through systematic investing. You’re joining a savvy community that understands starting now beats waiting for perfect conditions.

Don’t overthink it. Don’t put it off until “someday.” Your future self, enjoying financial independence, will thank you for starting today.

Start your automatic investment journey. You’ve got this!

Disclaimer: Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. This content is for educational purposes only and does not constitute financial advice. Consider your personal circumstances and consult with a qualified financial advisor before making investment decisions. Tax treatment depends on individual circumstances and may change.

Table of Contents

- 15 Best AI Tools to Save Money in 2026 and Cut Everyday Expenses

- Best Foods for Brain Health: 15 Science-Backed Choices to Boost Memory

- FIFA World Cup 2026

- How to Start a Side Hustle While Working a Full-Time Job

- Side Hustles for Moms: Earn Money From Home in 2026

Thank you for your feedback! We appreciate you taking the time to read the article. We’d be happy to explain…

Thank you for your feedback! We appreciate you taking the time to read the article. We’d be happy to explain…

Thank you for your feedback! We appreciate you taking the time to read the article. We’d be happy to explain…

Thank you for your feedback! We appreciate you taking the time to read the article. We’d be happy to explain…

Thank you so much! We’re really glad you found our point of view interesting and helpful. We appreciate your support,…

Leave a Reply