Budgeting Tools for Freelancers: Managing Irregular Income

Freelancers and gig workers worldwide continue to face the feast-or-famine cycle of unpredictable pay — and in 2026, that challenge is more widespread than ever. According to a recent Upwork Future of Work Report, over 1.57 billion people globally now participate in freelance or gig-based work, a figure that has grown sharply since the post-pandemic remote work boom.

By definition, irregular (variable) income means your earnings can shift dramatically from month to month, whether you’re a designer in New York, a developer in New Delhi, or a content creator in Nairobi — which is precisely why finding the best budgeting tools for freelancers with irregular income 2026 has become one of the most searched financial questions among the self-employed. As NerdWallet explains, variable income doesn’t just require a different mindset — it requires an entirely different financial system.

This unpredictability makes budgeting uniquely challenging in ways that traditional personal finance advice simply doesn’t address. Most budgeting frameworks were designed for salaried workers with a fixed paycheck, so when freelancers try to apply them, it often feels, as many describe it, “like a nightmare” — one month is flush with income, and the next, basic bills become a struggle. In 2026, inflation in key freelance markets like the US, UK, and India has added another layer of pressure, with Investopedia’s 2025–2026 Cost of Living Index showing that variable-income earners are disproportionately affected by rising housing and software subscription costs.

This is why the conversation around the best budgeting tools for freelancers with irregular income 2026 has shifted from simple expense tracking to full income-smoothing and cash-flow forecasting. For a practical visual overview of how freelancers are adapting, this YouTube breakdown is a great starting point: 📹 How Freelancers Should Budget in 2025/2026 — Step by Step.

To truly thrive in today’s gig economy, self-employed professionals need disciplined, tech-assisted money management that accounts for both dry spells and windfall months. The best budgeting tools for freelancers with irregular income 2026 are no longer just spreadsheets or basic apps — they now include AI-powered cash flow predictors, automated tax-savings buckets, and real-time invoice tracking dashboards. Platforms like YNAB (You Need a Budget), FreshBooks, and Copilot Money have all released significant 2026 updates specifically targeting freelancers, adding features like income variability alerts and rolling 90-day budget projections.

According to Forbes Advisor’s 2026 Budgeting App Roundup, the most effective tools for variable-income earners are those that separate “baseline survival budgets” from “surplus allocation” — a distinction that traditional apps long ignored. For a deeper dive into how these tools compare in real use, this video is highly recommended: 📹 Best Budgeting Apps for Freelancers 2026 — YNAB vs. Copilot vs. FreshBooks.

This guide covers self-employed budgeting strategies and reviews the best budgeting tools for freelancers with irregular income 2026, blending authoritative financial research with practical, on-the-ground advice. Drawing from sources like the IRS Self-Employed Tax Center, MoneySavingExpert, and the Global Freelancer Finance Survey 2026, we’ll walk through why budgeting is structurally harder for freelancers, explore step-by-step income-smoothing strategies applicable globally, and review the top apps that make tracking variable income not just manageable — but genuinely empowering. Whether you’re a seasoned independent contractor or just stepping away from a salaried role, understanding the best budgeting tools for freelancers with irregular income 2026 could be the single most impactful financial decision you make this year.

Why Budgeting Is Hard for Freelancers

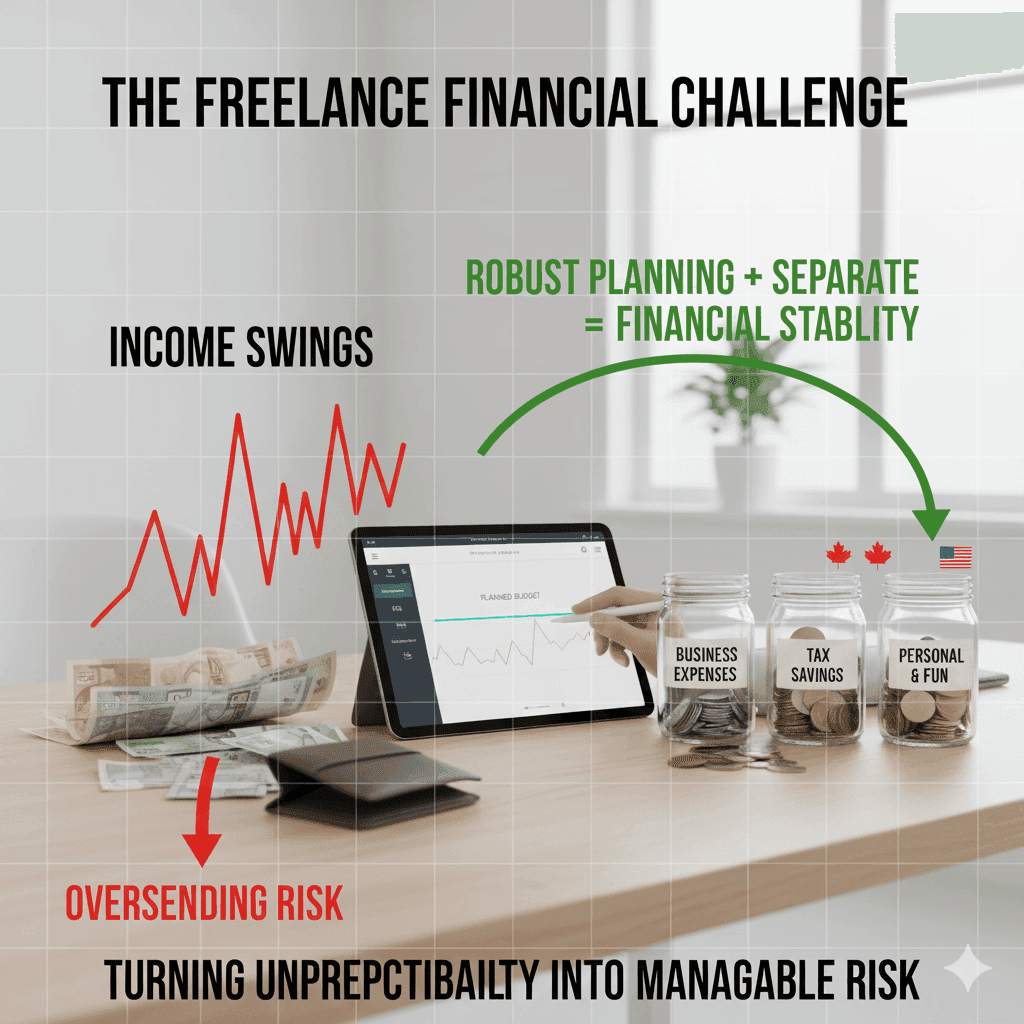

For traditional employees, a set paycheck arrives like clockwork — and that predictability is the invisible foundation of every mainstream budgeting strategy ever written. Freelancers, by contrast, operate without that safety net, and in 2026 the financial gap between salaried workers and independent professionals has never been more visible. Income swings — landing a high-value project one month, waiting on a late-paying client the next — create compounding planning headaches that no simple spreadsheet can solve.

This is exactly why demand for the best budgeting tools for freelancers with irregular income 2026 has surged, with app downloads in the personal finance category among self-employed users rising by nearly 34% year-over-year, according to Statista’s 2026 Fintech Usage Report. Without a fixed paycheck as a baseline, it becomes dangerously easy to overspend during flush months and then scramble to cover even basic expenses during lean periods — a cycle that quietly erodes both financial stability and mental well-being. For a clear visual breakdown of why freelance income patterns are so uniquely difficult to manage, this video is an excellent starting point: 📹 Why Freelancers Struggle to Budget — And How to Fix It (2026).

According to leading financial experts at Investopedia and NerdWallet, the inherent income volatility of freelance work means that “robust budgeting” is not optional — it is the single most critical financial habit a self-employed professional can build. The right tools in 2026 go far beyond simple expense tracking. The best budgeting tools for freelancers with irregular income 2026 now deliver predictive cash flow modeling, automated tax reservation (typically 25–30% set aside per deposit), and real-time alerts when monthly income falls below a user-defined survival threshold.

These capabilities transform budgeting from a backward-looking record of what you spent into a forward-looking system that tells you what you can safely spend — and that distinction is everything when your income arrives in unpredictable waves. The Federal Reserve’s 2025 Report on the Economic Well-Being of US Households found that freelancers with structured budgeting systems were 2.4 times more likely to report financial confidence compared to those without one, reinforcing that tools and discipline together are the real solution.

Freelancers worldwide report strikingly similar struggles regardless of geography, and the 2026 data confirms this is a global phenomenon. A widely cited Canadian financial planning study from the Financial Consumer Agency of Canada notes that irregular income “often leads to stress or overspending during lean months,” underscoring the need for flexible, adaptive budgeting frameworks rather than rigid monthly plans.

In the United States specifically, a growing number of freelancers are managing variable cash flow by maintaining multiple FDIC-insured bank accounts — a practice now actively recommended by the Consumer Financial Protection Bureau (CFPB) as a foundational step for gig workers. Separating a “bills account,” an “emergency buffer account,” and an “income holding account” adds an extra layer of financial security and eliminates the psychological trap of spending money that is already mentally earmarked for taxes or rent. In fact, account-separation strategies are now built directly into several of the best budgeting tools for freelancers with irregular income 2026, with apps like YNAB and Monarch Money offering automated bucket-splitting features as of their 2026 updates.

📹 How to Set Up Separate Bank Accounts as a Freelancer — 2026 Guide.

The challenge of freelance budgeting is universal, but a disciplined approach paired with the right technology genuinely transforms unpredictability into manageable, even plannable, risk. Whether you’re a designer in Lagos, a developer in Berlin, or a writer in Chicago, the best budgeting tools for freelancers with irregular income 2026 give you the insight to plan not just your monthly bills, but your savings targets, quarterly tax payments, and yes — even vacations — with real confidence.

If you’re also looking to diversify and grow your freelance income streams alongside better budgeting, this practical guide on earning online with zero upfront investment breaks down seven beginner-friendly methods that can help you generate $500+ monthly — a useful complement to any budgeting strategy, because the best financial system works even better when paired with a growing income.

Key Budgeting Strategies for Freelancers

Here are your updated paragraphs:

Key Budgeting Strategies for Freelancers

To tame irregular cash flow in 2026, the foundation hasn’t changed — but the tools, benchmarks, and expectations around each strategy have evolved significantly. Today’s freelancers aren’t just managing money; they’re building adaptive financial systems designed to absorb unpredictability without sacrificing stability. Whether you’re just starting out or refining a system that’s worked for years, these strategies represent the backbone of what the best budgeting tools for freelancers with irregular income 2026 are built to support. Let’s walk through each one carefully, because understanding the why behind each strategy is just as important as the how.

Calculate a Realistic Baseline Income

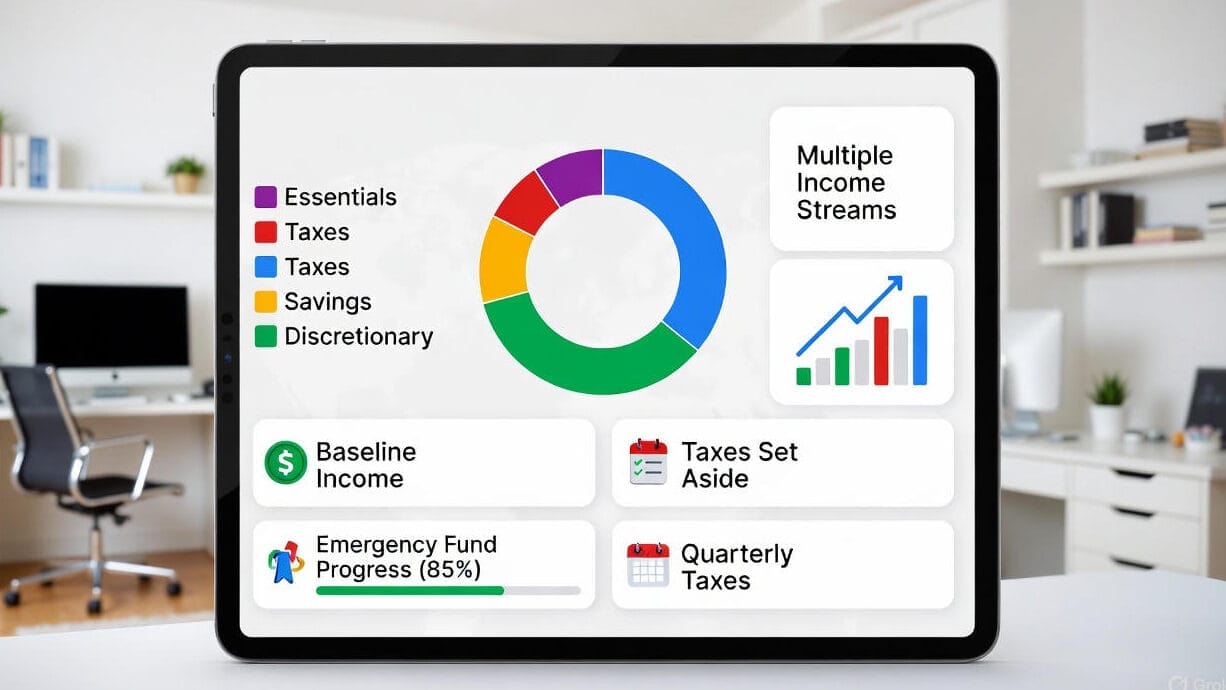

The very first step is knowing your average monthly income — not your best month, not your worst, but a realistic middle ground. To calculate it, sum your total earnings across the past 6 to 12 months from all gigs, retainer clients, and side projects, then divide by the number of months. If your total freelance income last year was $60,000, your baseline is $5,000 per month. However, a more conservative — and arguably smarter — approach recommended by Investopedia’s 2026 Freelancer Finance Guide is to use your lowest-earning month as the baseline rather than the average.

This creates a built-in buffer for slower periods and protects you from the psychological trap of planning around your best months. The best budgeting tools for freelancers with irregular income 2026, such as YNAB and Copilot Money, now automate this calculation by analyzing your connected bank history and suggesting a conservative income baseline for you — a feature that would have required a financial advisor just five years ago. 📹 How to Calculate Your Baseline Income as a Freelancer — 2026

Prioritize Essentials Above Everything Else

Once you have your baseline, the next move is to lock in your non-negotiable fixed costs before a single dollar is assigned anywhere else — rent or mortgage, utilities, insurance premiums, loan repayments, childcare, and any subscription services critical to your work. Upwork’s 2026 Financial Wellness Report for Freelancers recommends listing every must-pay expense as the very first layer of your budget, treating them with the same seriousness as a payroll obligation.

The practical trick here is to transfer the exact amount needed for these essentials into a dedicated “bills account” the moment any income lands — before it gets absorbed into daily spending. This approach is now a standard feature in the best budgeting tools for freelancers with irregular income 2026, with apps like Monarch Money and Simplifi by Quicken offering automatic “essential expense lock” modes as part of their 2026 feature rollouts.

Build a Freelancer Emergency Fund — Bigger Than You Think

Traditional financial advice recommends a 3-to-6-month emergency fund, but for freelancers navigating the 2026 economy — where inflation in the US, UK, Canada, and Australia remains elevated above pre-pandemic norms — most financial planners are now recommending 6 to 9 months of living expenses as the new standard, according to Forbes Advisor’s Emergency Fund Guide 2026. This fund should live in a high-yield savings account completely separate from your operating funds — not just for discipline, but because the average high-yield savings account in 2026 is offering 4.5–5.1% APY, meaning your buffer actively grows while it waits.

Set up an automatic transfer of 10–20% of every payment you receive directly into this account, treating it as a non-negotiable line item rather than an optional extra. As one financial expert puts it, for irregular income earners, an emergency fund is not a luxury — it’s a survival necessity. The best budgeting tools for freelancers with irregular income 2026 make this automatic, with YNAB’s “Age Your Money” feature and FreshBooks’ cash reserve alerts both designed specifically to help freelancers build this cushion without thinking about it. 📹 Emergency Fund Strategy for Freelancers 2026 — How Much Is Enough?

Separate Business and Personal Finances Ruthlessly

One of the most damaging mistakes freelancers make is running personal and business money through the same account — it creates tax chaos, distorts your true financial picture, and makes it almost impossible to budget accurately.

The solution is to maintain at minimum three separate accounts: a business income account where all client payments land, a personal spending account that receives your “salary” transfer, and a dedicated tax reserve account where you automatically park 25–30% of every payment (the IRS-recommended self-employment tax buffer, outlined in the IRS Self-Employment Tax Guide). In the US, keeping these funds in FDIC-insured accounts adds an additional layer of security, protecting up to $250,000 per depositor per institution. This account-separation strategy is now deeply embedded in the best budgeting tools for freelancers with irregular income 2026 —

Wave, FreshBooks, and QuickBooks Self-Employed all offer automated tax-bucket features that pull the correct percentage from every deposit the moment it arrives.

Pay Yourself a Consistent Pseudo-Salary

This is one of the most psychologically powerful strategies a freelancer can adopt, and it’s gaining significant traction in 2026 as more independent workers seek stability without sacrificing the freedom of freelancing. The idea is straightforward: based on your conservative baseline income, decide on a fixed monthly “paycheck” to transfer from your business account to your personal account — say, $4,000 per month even if you earned $7,000 that month.

The surplus stays in the business account as a forward buffer for slower months. This creates a lived experience of financial consistency, even when your actual client income is anything but consistent. NerdWallet’s 2026 Self-Employment Guide describes this as one of the top behavioral finance strategies for reducing freelancer financial anxiety, and the best budgeting tools for freelancers with irregular income 2026 increasingly build this salary-simulation feature directly into their dashboards.

Apply a Structured Budgeting Rule to Every Dollar

Rather than spending reactively, assign every dollar a job the moment it arrives. Two frameworks dominate in 2026. The classic 50/30/20 rule allocates 50% to essential living costs, 30% to business or discretionary spending, and 20% to savings and investments — a framework well-suited to freelancers with moderate income variability.

For those with wilder swings, Upwork’s 2026 Financial Guide recommends the 70/20/10 split: 70% to essential expenses, 20% to savings and tax reserves, and 10% to discretionary or reinvestment. Either approach works — the critical point is consistent pre-assignment. The best budgeting tools for freelancers with irregular income 2026 automate this allocation the moment income is detected, removing the willpower requirement entirely. 📹 50/30/20 vs 70/20/10 Budget Rule — Which Works Best for Freelancers in 2026?

Track Every Single Dollar — Without Exception

Rigorous, consistent tracking is the nervous system of a healthy freelance budget. Recording every income source and expense, no matter how small, builds the financial self-awareness that makes all other strategies possible. As one widely cited freelancer guide explains, observing income and expense patterns helps you identify your real “budget anchors” — the recurring inflows and outflows that define your true financial baseline. In 2026.

this process has been almost entirely automated through the best budgeting tools for freelancers with irregular income 2026, with apps like Copilot Money, Monarch Money, and Tiller using AI-driven categorization to log and sort transactions in real time — no manual entry required. Well-organized tracking also transforms tax season from a stressful scramble into a straightforward process, with Upwork’s bookkeeping guide and the IRS’s recordkeeping recommendations for self-employed individuals both emphasizing that detailed income and expense records are your single best defense in the event of an audit.

Here are your fully updated paragraphs:

Top Budgeting Apps and Tools

The landscape of personal finance software has evolved dramatically, and in 2026 freelancers have access to a richer, smarter toolkit than ever before. The best budgeting tools for freelancers with irregular income 2026 are no longer simple expense loggers — they are intelligent financial systems that predict cash flow, automate tax reserves, flag income gaps before they become crises, and in many cases learn your spending patterns through AI. Below is a thorough, updated review of the most powerful and widely used options available globally and in the US, designed to help you match the right tool to your specific freelance situation. 📹 Best Budgeting Apps for Freelancers 2026 — Full Comparison

YNAB – You Need A Budget (Paid, ~$109/year – Global)

YNAB remains one of the most consistently recommended of all the best budgeting tools for freelancers with irregular income 2026, and for good reason — its entire philosophy is built around the reality that income arrives in unpredictable chunks rather than neat monthly deposits. The core mechanic is zero-based budgeting: every dollar of income you receive is immediately assigned to a specific category — rent, taxes, emergency fund, subscriptions, food — before it can be spent unconsciously.

For freelancers, this is transformative, because it forces you to make intentional decisions about windfall months rather than letting the extra money dissolve into lifestyle inflation. YNAB’s 2026 update introduced an “Irregular Income Mode” that builds a rolling 90-day income average and adjusts your budget categories proportionally, which is exactly the kind of feature that separates purpose-built freelancer tools from generic budgeting apps. According to YNAB’s own user research, new users save an average of $600 in their first two months — a figure that likely underestimates the impact for variable-income users who previously had no system at all. The annual cost is fully justified for anyone serious about financial stability.

QuickBooks Self-Employed (Paid, ~$20/mo – US/Global)

For freelancers who need budgeting and full business accounting in a single platform, QuickBooks Self-Employed continues to be one of the most capable of all the best budgeting tools for freelancers with irregular income 2026. It connects directly to your business bank accounts, automatically categorizes income and expenses, tracks mileage via your phone’s GPS, and — crucially — estimates your quarterly self-employment tax liability in real time so you always know exactly how much to reserve. The IRS requires self-employed individuals earning more than $1,000 annually to file quarterly estimated taxes, and QuickBooks’ automated reminders and calculations make this one of the least stressful parts of freelance finances.

Its 2026 integration with Intuit’s AI assistant allows freelancers to ask plain-English questions like “Can I afford a new laptop this month?” and receive answers grounded in actual account data. For freelancers working with international clients, pairing QuickBooks with a cross-border payment platform like Wise Business or Payoneer is widely recommended to eliminate currency conversion delays that distort cash flow tracking. 📹 QuickBooks Self-Employed 2026 — Full Setup Guide for Freelancers

Wave (Free – US/Canada)

Wave remains one of the most remarkable free tools in the entire freelance finance ecosystem, and its 2026 feature set has expanded meaningfully. It functions as a complete small-business accounting platform — invoicing, payment collection, income tracking, and basic expense management — all at no cost for its core features.

While Wave isn’t an envelope-style budgeting app, it serves as an excellent financial foundation layer that many freelancers pair with a dedicated budgeting tool like YNAB or Copilot. The combination of Wave for bookkeeping and YNAB for active budget management is a popular “two-tool system” among freelancers mentioned across forums like Reddit’s r/freelance and endorsed in NerdWallet’s freelancer finance guides. For Canadian freelancers specifically, Wave’s native support for CAD, GST/HST tracking, and CRA-compatible expense categories makes it particularly well-suited to the local tax environment.

Copilot Money (Paid, ~$95/year – US, iOS/Mac)

Copilot is arguably the most visually polished and AI-forward of all the best budgeting tools for freelancers with irregular income 2026, and it has gained significant traction among creative freelancers who want deep financial insight without the complexity of accounting software. Its machine-learning transaction categorization is among the most accurate available in 2026, learning your specific spending patterns over time and reducing the need for manual corrections to near zero.

Copilot’s “Projected Balance” feature — which forecasts your account balance weeks into the future based on known recurring expenses and income patterns — is especially valuable for freelancers managing cash flow anxiety. According to Forbes Advisor’s 2026 Budgeting App Review, Copilot earned top marks for user experience and AI-driven insights among variable-income users. Its current limitation is that it is iOS and Mac only, so Android users will need to look elsewhere for a comparable experience.

PocketGuard (Free/Paid – US)

PocketGuard earns its place among the best budgeting tools for freelancers with irregular income 2026 through its beautifully simple answer to the question every freelancer asks constantly: how much can I actually spend right now? After you connect your accounts, PocketGuard deducts your upcoming bills, reserved savings, and tax allocations from your current balance and shows you a single, clear number labeled “In My Pocket.” For freelancers prone to overspending during high-income months because everything feels fine, this simple visual guardrail is genuinely protective.

PocketGuard Plus (the paid tier) adds custom budget categories, debt paydown planning, and subscription cancellation tools — the latter being increasingly valuable as subscription costs have crept upward across 2025 and 2026. Investopedia’s app review describes it as one of the most accessible entry points for freelancers new to structured budgeting.

Monarch Money (Paid, ~$99/year – US/Canada)

Since Mint’s closure in early 2024, Monarch Money has emerged as one of the most popular replacements and is now firmly established among the best budgeting tools for freelancers with irregular income 2026. It combines a clean net worth dashboard, flexible budget customization, collaborative features for freelancers who share finances with a partner, and one of the best cash flow visualization tools currently available.

Its “Recurring Transactions” detection is particularly useful for freelancers who need to quickly distinguish their variable project income from stable retainer payments. The Verge’s 2026 personal finance app guide named Monarch Money the top overall budgeting app for users migrating from Mint, and its active development team has been consistently releasing freelancer-specific features throughout 2025 and into 2026. 📹 Monarch Money Full Review 2026 — Best Mint Alternative for Freelancers?

Goodbudget (Free/Paid – Global)

For freelancers who prefer a more hands-on, intentional approach to money management, Goodbudget’s digital envelope system offers something the more automated apps cannot — the psychological engagement of manually deciding where every rupee, dollar, or pound goes. You set up envelopes for each spending category and allocate funds to them at the start of the period; as you spend, the envelopes deplete visually.

This manual element, while seen as a limitation by some, is actually a feature for freelancers who want to build stronger financial intuition rather than simply automate their way to stability. Goodbudget is also one of the few truly global options on this list, working equally well in the US, UK, India, Nigeria, and beyond, with no regional bank connection restrictions since it operates on manual entry rather than direct account linking.

Regional Tools — India, Africa, and Emerging Markets

The best budgeting tools for freelancers with irregular income 2026 aren’t exclusively Western products, and it’s important to acknowledge the strong regional options serving freelancers in India and other high-growth gig economies. For Indian freelancers, ET Money and Walnut have both updated significantly, offering INR-native categorization, UPI transaction tracking, and automated GST-friendly expense separation. Groww and Scripbox integrate savings and investment automation directly, letting freelancers set predefined “buckets” for SIP investments, emergency reserves, and tax advance payments simultaneously.

For African freelancers, platforms like Kuda Bank (Nigeria) and M-PESA integrated budgeting tools (Kenya) have matured into full financial management ecosystems that now rival Western equivalents in functionality. These regional tools matter because the freelance boom in 2026 is truly global, and the best financial tool is always the one that speaks your currency, understands your local tax system, and connects to your local bank.

Spreadsheets — Google Sheets, Excel, and Notion (Free/Global)

No list of the best budgeting tools for freelancers with irregular income 2026 would be complete without acknowledging the enduring power of a well-built spreadsheet. For analytically minded freelancers who want total flexibility, a custom Google Sheets or Excel workbook — built around zero-based budgeting or an envelope template — remains one of the most powerful and customizable financial systems available.

The upside is complete control: you can track exactly what matters to you, build your own income forecasting formulas, and design dashboards that reflect your unique cash flow patterns. Notion has also gained significant traction as a hybrid productivity-and-finance workspace, with a thriving community of freelancers sharing income tracking templates on Notion’s template gallery. The honest downside is the manual effort required — but for those willing to invest the time, no app will ever give you a more precise picture of your own finances. Tiller Money bridges the gap beautifully in 2026, automatically feeding real bank data into Google Sheets templates, combining the flexibility of a spreadsheet with the convenience of automated data sync.

Taken together, these tools represent a genuinely diverse ecosystem of options, and the right choice depends entirely on your income level, geographic location, technical comfort, and whether you prioritize automation or intentional manual control. The most important insight is this: the best budgeting tools for freelancers with irregular income 2026 are the ones you will actually use consistently — because even the most sophisticated app in the world only works if it becomes a daily habit.

By combining these seven strategies — baseline calculation, essentials prioritization, emergency buffering, account separation, pseudo-salary discipline, proportional allocation, and meticulous tracking — freelancers in 2026 can genuinely convert the chaos of variable income into a manageable, even empowering, financial rhythm. Each strategy becomes significantly more effective when supported by the best budgeting tools for freelancers with irregular income 2026, because the right tools don’t just record your financial life — they actively shape and protect it.

Each tool has its strengths. Mint and Pocket Guard shine for ease-of-use, YNAB for strict budgeting discipline, and QuickBooks/Wave for integrated accounting. As one freelancer blog notes, whether you use “Mint, YNAB, or QuickBooks, each offers unique benefits” to simplify your budgeting process..

Step-by-Step Budgeting Guide

Putting it all together, here’s a numbered step-by-step process to budget as a freelancer or self-employed person:

- Calculate Your Baseline Income: Total your earnings for the past 6–12 months and divide by the number of months. This is your baseline monthly income. Use the most conservative figure (e.g. the lowest-earning month) for safety. This will be the foundation of your budget each month.

- List and Prioritize Expenses: Write down all your monthly expenses and categorize them as essential (fixed) or variable. Essential items (rent, utilities, loan payments, insurance) must be paid first. Variable costs (groceries, utilities, fuel, supplies) can fluctuate. Plan to cover fixed costs out of your baseline immediately, then see what’s left for variable spending. One simple rule is the 70% rule: plan to spend 70% of your expected income on essentials and savings, keeping 30% flexible.

- Assign Money into Buckets: Now that you have categories, allocate portions of your income to each bucket. For example: X% to housing and bills, Y% to food/transportation, Z% to business reinvestment, etc. A commonly used framework is 50/30/20 (essentials/savings/discretionary) or Upwork’s 70/20/10 rule. The exact split depends on your situation. The key is that every dollar of income gets a job. Use a budgeting app or envelope system (digital or cash envelopes) to enforce these allocations.

- Build Your Emergency Fund: Each month, put a set amount (e.g. 10–20% of income) into a separate savings account for emergencies. Treat this transfer like a fixed expense. If you have a very good month, move even more into savings. The goal is to reach at least 3–6 months’ worth of basic expenses saved. This fund ensures that if a month falls short, you can cover costs without debt.

- Automate and Track: Use technology to help. Automate bill payments and savings transfers as much as possible. In your budgeting app or spreadsheet, record every source of income (project payments, side gigs) and every expense. Modern apps can even scan receipts and tag expenses with a client or project. Seeing all transactions in one place (dashboard or spreadsheet) gives you insight into spending patterns. Review this data monthly: look for leaks (subscription you don’t need, overtime on dining out, etc.) and adjust categories as needed.

- Set Aside Money for Taxes: Freelancers often owe taxes quarterly. Decide on a tax percentage (e.g. 20–30%) and move that amount into a dedicated tax account each time you’re paid.

- Budgeting tools with tax features (like QuickBooks Self-Employed) can estimate this automatically. That way, tax season won’t wreck your budget: you’ll have the cash ready for IRS or other tax payments.

- Grow Multiple Income Streams: Instead of relying on one client or gig, look for additional income sources (consulting, side projects, affiliate revenue, etc.). Having multiple streams smooths out feast-famine swings. As Transfi advises, seek retainer clients or passive income opportunities for stability. More income sources mean more ability to follow your budget comfortably.

- Review and Adjust: At the end of each month, compare your actual spending to your budget. Did you overspend in any category? Did you save enough? Use these insights to tweak next month’s allocations. Budgeting is an ongoing process. Even the best plans need adjustments when life changes (new expenses, increased rates, etc.). The most successful freelancers regularly check their budgets and adjust targets for the next month.

By following these steps, you create a flexible budget that adapts to ups and downs. Remember, the goal is long-term stability, not perfection every month. Even if you occasionally dip into savings, staying on track overall prevents crisis.

Choosing and Using the Right Budgeting Tool

With strategies in place, pick a tool that fits your style and needs:

- Flexibility vs. Simplicity: Some freelancers need rich features (project tags, integration with bank accounts) and don’t mind a learning curve. Others want something extremely simple. An expert tip: “the best tool is the one you’ll actually use consistently”. If a complex app feels overwhelming, try a simpler one or even a spreadsheet. Conversely, if you love data, a full-featured app or accounting suite might keep you engaged.

- Expense Tracking: Look for apps with easy expense input. As one guide points out, mobile apps with receipt scanning (OCR) and the ability to tag expenses by client/project are a huge time-saver. This is crucial for maximizing deductions and understanding your cash flow. If you use cash or small payments, choose an app that quickly logs those. Mint and QuickBooks, for example, let you snap receipts on your phone.

- Income Tracking: The app should let you record variable income easily. You’ll want to tag each payment (by client or project) and date it. Some tools (like PocketGuard) automatically pull income from linked accounts and label it. This visibility helps you forecast upcoming months. Always ensure your tool can handle multiple income sources without confusion.

- Tax Support: Consider whether the tool assists with taxes. QuickBooks Self-Employed and FreshBooks can estimate taxes; Mint shows your overall net income; even Google Sheets can incorporate tax calculations. At minimum, your budget should remind you to save for taxes. If you live in a country with complicated self-employment tax (like the US), a tool with tax reports can be worth it.

- Integration: Can it connect to your bank, credit cards, PayPal or invoicing software? Integration means less manual entry. For instance, Wave and QuickBooks sync with bank feeds; YNAB and Mint link to accounts; even PocketGuard pulls data from your bank. This automation cuts errors and saves time. Also check if it can export data – useful if you hire an accountant or need reports.

- Security and Accessibility: Make sure the tool is secure (bank-level encryption is a must) and that you can access it on all your devices (phone, web). Being able to check your budget on the go helps you stick to it. Many apps offer password protection or even biometric login.

- Cost: There are free and paid options. If budget is tight, start with free tools (Mint, Goodbudget, or Google Sheets). If you have a decent income, investing in a paid app (YNAB, QuickBooks, PocketGuard Premium) can pay off by saving you time.

In short, compare features side-by-side. As one financial blog advises, look at income/expense categorization, reporting capabilities, and user interface. A cluttered interface may mean you stop using it. Read reviews from other freelancers. After all, the goal is not just to record what happened, but to plan ahead and change financial habits. The right tool will become your financial “co-pilot,” guiding you to save during peaks and spend wisely during valleys

Global and US Considerations

While the above advice is broadly applicable, here are a few regional notes:

- Global Freelancers: Wherever you are, the same principles hold: calculate a baseline, save a buffer, track every payment. Currency differs, but apps like Mint and YNAB support multiple currencies. If you deal with multiple currencies, look for tools that can consolidate or report in your main currency. Many budgeting tools are globally available. For example, Transfi’s list of tools includes Indian-specific apps (Walnut, Scripbox/Groww) because they handle rupees and local investment norms. Freelancers in Europe or Asia may find local versions or use global apps with localization settings. In any country, keeping an emergency fund and separating accounts is crucial.

- United States: U.S. freelancers can take advantage of tax-optimized tools. QuickBooks Self-Employed and TurboTax Self-Employed integrate well with US tax rules. Also, FDIC insurance only applies to US banks; Upwork recommends multiple FDIC-insured accounts (for checking, savings, taxes) to keep money safe and organized. Credit Karma (free credit monitoring) is US-specific and can track your spending at US banks. Apps like PocketGuard and YNAB have strong user bases in the US.

In sum, adapt the basics to your location. The budgeting tools may vary (Mint is US/Canada only, whereas Goodbudget is global, etc.), but the strategies (baseline budgeting, emergency funds, expense tracking) are universal.

Image: A freelancer at a home office, working through budgeting paperwork and tools. Freelancers often manage their own finances from a home workspace, tracking income and expenses carefully. (Source: Kaboompics/Pexels)

Conclusion: Financial Freedom for Freelancers

Budgeting doesn’t have to be another source of stress for freelancers – with the right plan and tools, it can become your superpower. By embracing disciplined budgeting strategies (baseline income, emergency funds, savings buckets) and leveraging apps built for irregular income, you transform uncertainty into control. As one guide puts it, once you start using these tools, “managing your finances is not just possible – it’s also rewarding!”. You’ll gradually feel less anxious about slow months and more confident about future goals (like a new computer or vacation).

Whether you pick YNAB or Mint, Wave or a custom spreadsheet, the key is consistency. Regularly review your budget, adjust as needed, and stick to the plan during both feast and famine. Global freelancers and US freelancers alike can apply these methods, just tailored to local currency and banking nuances. In the end, the right tools and mindset let you focus on your work – and enjoy the freedom of freelancing – without being overwhelmed by finances. Start today: set up a simple budget, choose an app or spreadsheet, and take the first step toward financial stability and freedom.

“This article is created through ongoing research, trend analysis, and careful fact-checking to keep our readers informed. Every detail shared is taken from reliable and updated information available across the web. Our goal is to provide freelancers with practical, trusted guidance they can apply in real life.”